Author: QSV Equity

QSV Equity Investors Q4 2022 Commentary

QSV Equity Investors

Q4 2022 Commentary

Q4 2022 began with a bear market rally that continued into November but waned in December. Rate hikes

by the Federal Reserve and Chairman Powell’s comments that it was too soon to consider a pause tested

investors’ resolve. November’s mid-term election delivered the ingredients for gridlock in Washington,

and we ended 2022 with investors feeling the sting of a difficult year that offered few places to hide from

sharply negative results.

The exceptional place to hide for equity investors in 2022 was the energy sector. QSV has generally

found few businesses in this sector that we believe make prudent capital allocation decisions and our

underweight to these companies was a meaningful drag on our annual performance.

QSV’s Quality Value Smallcap strategy did produce returns ahead of both the Russell 2000 Value and

Russell 2000 indices in 2022. Our Quality Value Midcap and Select Value strategies each lagged their

respective Russell value indexes while outperforming the Russell Mid Cap and Russell 2500 indexes,

respectively. We remain confident in our ability to outperform these benchmarks over full market cycles

and have done so since the inception of each product. More information including since-inception

performance for each of the strategies may be found at www.qsvequityinvestors.com.

QSV Strategy Quarterly Performance

The QSV Quality Value Smallcap Strategy returned 6.58% and 6.49%, gross and net of fees, lagging

the Russell 2000 Value Index return of 8.42% while leading the Russell 2000 Index return of 6.23%. Security

selection in Healthcare and Energy helped performance, while an underweight and negative security

selection in Consumer Discretionary companies detracted.

Quality Value Smallcap Top Contributors

Rocket propulsion supplier Aerojet Rocketdyne Holdings Inc. (AJRD) was the leading contributor to

performance during the quarter. Shares rose nearly 40% on news that the company would be acquired by

L3Harris Technologies (LHX) after AJRD was courted by multiple suitors. Earlier in 2022, an acquisition of

the company by Lockheed was scuttled over antitrust concerns. We continue to hold AJRD and believe

the likelihood that the deal will close in early 2023 is high.

Shares of property and casualty insurer RLI Corp. (RLI) rose more than 35%. Despite the impact of

Hurricane Ian, RLI quarterly results were strong, with lower-than-expected losses and a 13% increase in

gross premiums written. Earnings reflected the gains on the sale of RLI’s minority ownership in eyewear

maker Maui Jim for $686 million, a stake held for more than 25 years due to RLI’s legacy ophthalmic

services subsidiary.

Quality Value Smallcap Top Detractors

Simulations Plus Inc. (SLP) was the leading detractor to performance for the quarter as shares dropped

on earnings that were below street expectations. SLP is a leading provider of software and services used

by major pharmaceutical, biotech, and regulatory agencies to make better informed, data-driven

decisions. While earnings are expected to be more muted in the coming year due to higher labor costs,

we see long term value due to the company’s high switching costs, intellectual assets, and a 93% renewal

rate by its customers. SLP produces operating margins of 29% on average and its shares are well below

our estimate of intrinsic value.

Shares of direct-to-consumer pool and spa provider Leslies Inc. (LESL) fell during Q4 on recession concerns

and worries over consumer spending. LESL is the industry leader globally, with both physical stores and

strong digital distribution, and benefits from recurring revenues from meeting its customers’ maintenance

needs. While we have confidence in its business model, we sold our position in LESL for better

opportunities.

Quality Value Smallcap Portfolio Activity

With the early quarter rally and subsequent decline, QSVsaw many opportunities to upgrade its

portfolio. QSV exited positions in Allied Motion Technologies (AMOT), CarGurus Inc. (CARG), Leslies

Inc. (LESL), and John B. Sanfilippo and Son Inc. (JBSS).

New positions were initiated in title and specialty insurer First American Financial (FAF), home generator

manufacturer Generac Holdings (GNRC), exploration and production company PDC Energy (PDCE), and

UFP Industries (UFPI), a provider of lumber and treated wood products.

The QSV Quality Value Midcap Strategy returned 9.03% and 8.76%, gross and net of fees, for the

quarter, lagging both the Russell Mid Cap Value Index return of 10.45% and the Russell Mid Cap Index

return of 9.18%. QSV’s security selection added value in the Energy and Consumer Staples sectors, while

security selection in Financial names detracted.

Quality Value Midcap Top Contributors

Ross Stores Inc. (ROST) rose by 38% during the quarter driven by strong Q3 results and optimism for the

coming quarter and 2023. Lower income consumers that drive sales for ROST have been challenged in

2022 by higher energy, housing, and food costs, but employment and wage growth appear as positives.

ROST is expected to continue to benefit from competitive advantages that include significant vendor

relationships and strong inventory management. Returns on invested capital stand at 30% on average.

Shares of management consulting firm Booz Allen Hamilton (BAH) rose during the quarter as the

company both beat quarterly expectations and raised guidance for revenue and earnings for the full year.

BAH is a leading provider of management and technology consulting. Its “best of breed” status stands as

a competitive advantage as it captures contracts from the U.S. government, generating 97% of the

company’s revenues. BAH generates returns on invested capital of 15% on average.

Quality Value Midcap Top Detractors

First Financial Bankshares Inc. (FFIN) shares fell as rising interest rates increased deposit costs and loan

demand moderated. FFIN is a highly profitable bank holding company with a footprint in the thriving Texas

market. FFIN produces returns on tangible equity of 16% and its shares are priced at a discount to our

view of its intrinsic value.

Shares of self-storage owner and operator Extra Space Storage (EXR) fell during the quarter as

management lowered earnings guidance. Lower share prices also reflected the impact of higher interest

rates; 38% of the company’s debt was variable at the end of Q3 2022. We continue to have confidence in

the long-term prospects for EXR, supported by its same-store occupancy rate of 96% and its size and scale,

giving it a significant cost advantage and marketing presence over smaller peers.

Quality Value Midcap Portfolio Activity

With the early quarter rally and subsequent decline, QSV saw many opportunities to upgrade its

portfolio. QSV exited Celanese Corp. (CE), Clorox (CLX), Take Two Interactive (TTWO), and Helen of

Troy (HELE).

New positions were initiated in exploration and production company APA Corp. (APA), industrial and

office REIT EastGroup Properties (EGP), Lennox International (LII), a leader in heating, ventilation and

cooling products, Northern Trust (NTRS), offering leadership in custody and wealth management services,

and Zebra Technologies (ZBRA), a leader in automatic identification and data capture technology.

The QSV Select Value Strategy returned 8.00% and 7.76%, gross and net of fees, trailing the return of

9.21% for the Russell 2500 Value Index while leading the return of 7.43% for the Russell 2500 Index. Select

Value is a high conviction strategy that takes QSV “best ideas” from our Quality Value Smallcap and

Quality Value Midcap strategies. Security selection helped performance most notably in Healthcare and

Industrials companies. An overweight and negative security selection in Information Technology

detracted from performance as did an underweight and negative security selection in Consumer

Discretionary names.

Select Value Top Contributors

Booz Allen Hamilton (BAH) was the leading contributor to performance during the quarter and is

discussed above.

Getty Realty Corporation (GTY) shares aided performance during the quarter as shares rose by over 27%.

The company met earnings expectations for the quarter and management raised guidance for the full year

2022. GTY owns a portfolio of more than 1000 properties that are leased at 99.5% with annual rent

escalators averaging 1.6%. Properties are predominantly convenience stores and gas stations which are

e-commerce and recession resistant.

Select Value Top Detractors

PubMatic Inc. (PUBM) was the leading detractor to performance during the quarter. PUBM is a leading

platform provider in the programmatic digital advertising technology market, helping publishers that

supply digital ad inventory to better manage their inventory, selling a high percentage of their inventory

and maximizing revenue per ad sold. Competitive advantages include switching costs – the time, effort,

and money required to transfer platforms once an advertiser is set up on PUBM’s platform – and cost

advantages through its investment in infrastructure and off-shore research and development. PUBM

produces returns on invested capital of 15% and its shares are currently at a significant discount to our

measure of intrinsic value.

National Storage Affiliates Trust (NSA) detracted from performance as rising interest rates are expected

to impact both the company’s variable rate debt and its borrowing costs for future acquisitions.

Additionally, occupancy rates were off more than anticipated. NSA is the fourth largest publicly traded

REIT focused on self-storage and benefits from high switching costs. We continue to have conviction in

high-quality NSA as it produces funds from operation well above its peers driven by its focus on properties

in secondary markets that are often overlooked by its competitors. While lower occupancies are cause for

concern, these levels follow post-COVID increases that were significant and unsustainable.

Select Value Portfolio Activity

Continuing with our approach to investing in the best ideas of QSV’s Quality Value Smallcap and

Midcap strategies, QSV sold and purchased several holdings, upgrading its portfolio. QSV exited

positions in Clorox (CLX), John B. Sanfilippo & Son (JBSS), Take Two Interactive (TTWO), and Helen of

Troy (HELE).

QSV initiated positions in EastGroup Properties (EGP), Generac Holdings (GNRC), PDC Energy (PDCE),

and Zebra Technologies (ZBRA) during the quarter.

Our Focus on the Long Term

The folly of predicting macro events was laid bare in 2022 as the Federal Reserve and Wall Street were

wildly wrong concerning the persistence of inflation and the direction of equity and bond markets. We

suspect that the Federal Reserve has more interest rate hikes in store for us in 2023, that a recession is

possible, that downward earnings revisions are likely, and that consumers face trouble as personal savings

rates are down while debt levels are up. To the positive, the employment picture remains strong, although

questions remain whether inflation can come down without impacting the labor market.

We know that the macro events of the coming year are unknowable, so, as always, we prepare for the

challenges and opportunities to come through ownership of quality businesses that possess competitive

“moats.” This approach has proven to be a cornerstone in building enduring wealth over the long term.

The price paid for ownership of these businesses is critical to success. There is great uncertainty as to the

outlook for corporate earnings in 2023 but we know that a focus on quality provides some clarity;

businesses with low leverage, stable and growing cash flows and stable and growing returns on invested

capital give us a far better starting point for making sound assessments of the future cash flows each

business will deliver. We believe the carnage of the past year has created tremendous opportunities to

upgrade to higher quality, small and mid-cap businesses, setting our clients up for success.

Disclaimer:

Returns are for the respective composites of QSV Equity Management (BEM). Gross returns are

calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s

management fee. All dividends are assumed to be reinvested. The returns of the BQV Midcap Strategy are

compared to the historical performance of the Russell Midcap Indices as they are a widely used

benchmarks for mid capitalization securities. The returns of the BQV Smallcap Strategy are compared to

the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small

capitalization securities. The returns of the QSV Select Value Strategy are compared to the historical

performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization

securities. An investment with QSV Equity Management should not be construed as an investment in a

program that seeks to replicate, or correlate with, these indices. Market conditions vary between the BEM

products and these indices. Furthermore, these indices do not include any transaction costs, management

fees and other expenses, as do the BEM Products. Lastly, BEM may invest in securities and positions that

are not included in these indices.

No client or potential client should assume that any information presented should be construed as

personalized investment advice. Personalized investment advice can only be rendered after engagement

of the firm for services, execution of the required documentation, and receipt of required disclosures.

Investing carries risk of loss.

QSV Equity Management, LLC claims compliance with the Global Investment Performance Standards

(GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote

this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a

GIPS report, please visit www.qsvequityinvestors.com.

QSV Equity Management, LLC is a registered investment advisor. For additional information about the

firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

QSV Equity Investors Q2 2022 Commentary

QSV Equity Investors

Q2 2022 Commentary

More information including since-inception performance for each of the strategies may be found at www.qsvequityinvestors.com.

Stocks were sharply lower during the second quarter of 2022, as persistently high inflation and the response from the Federal Reserve sparked worries over the severity of a resulting economic slowdown and risks of a recession. Consumers, the growth engine of the economy, showed fatigue as both their spending and savings rates waned in reaction to rising food and energy costs. Inflation hurt investor confidence and the visibility into future corporate earnings. While not immune to the selloff, stocks of higher quality companies weathered the downturn better than those of lower quality companies. Using the Russell Stability indexes as proxies for high and low quality, the Russell Defensive indexes containing businesses with higher Returns on Assets, lower leverage, and lower volatility significantly outperformed low quality businesses, as measured by the Russell Dynamic indexes, across the market cap spectrum.

Each of the QSV strategies outperformed its respective Russell indexes and each added value through stock selection during the quarter. Of note is the QSV Quality Value Smallcap strategy reaching its fifth anniversary, outperforming both the Russell 2000 Value and 2000 Indexes with less risk and positive stock selection over the five-year period.

QSV Strategy Quarterly Performance

The QSV Quality Value Smallcap Strategy returned -7.88% and -7.96%, gross and net of fees, leading the Russell 2000 Value Index return of -15.28% and the Russell 2000 Index return of -17.20%. Security selection in Healthcare, Industrials and Information Technology helped performance, while an underweight and negative security selection in Energy and an absence of Utilities companies detracted. QSV generally finds few businesses with high returns on invested capital in the Energy and Utilities sectors and these exposures are typical for our portfolios.

Quality Value Smallcap Top Contributors

UFP Technologies, Inc. (UFPT) was the leading contributor to performance during the quarter, as shares rose 20%. UFPT designs and manufactures products and packaging for customers in seven target industries including medical, automotive, aerospace, consumer, and industrial markets, using foams, plastics, composites, and natural fiber materials. The company produces returns on capital of 9% supported by its “medical centric” revenue mix that has high barriers to entry and is recurring in nature.

MGP Ingredients, Inc. (MGPI) shares rose on a strong earnings report during the quarter. MGPI manufactures distilled spirits and specialty wheat protein and food ingredients, operating through its Distillery Products and Ingredient Solutions segments. The Distillery Products business is more than fifty years old and produces whiskey, rye, bourbon, and vodka for the premium beverage market. In addition to its premium brands, MGPI gained over 100 spirits brands and national distribution capabilities in 2021 through its acquisition of Luxco. The company produces returns on invested capital of 17%.

Quality Value Smallcap Top Detractors

Shares of CarGurus (CARG) fell during the quarter, along with other online auto retailers, due to price volatility and softer retail sales. CARG offers a leading marketplace for both individuals and dealerships to buy, market and sell vehicles in the U.S. as well as Canada and the U.K. Asset light CARG has the competitive advantage of a strong network effect with over thirty-nine million unique visitors each month and over 30,000 paying dealerships globally. The company produces returns on invested capital of 16% and shares trade significantly below QSV’s view of intrinsic value.

Shares of energy services company Core Laboratories (CLB) fell during Q2 following robust returns in the first quarter. CLB is the singular energy holding in the QSV strategy and has competitive advantages that include its intangible assets (patents, proprietary technology, and human capital) and network effects (multi-client reservoir studies). Business performance has been negatively impacted as both COVID and the war in Ukraine have slowed exploration and production initiatives. Despite the headwinds to business performance, CLB produces returns on invested capital of 10% and we expect improvement to performance supported by strong commodity prices and consumer demand.

Quality Value Smallcap Portfolio Activity

Based on our conviction in certain holdings in the Quality Value Smallcap portfolio and on the valuations of certain stocks, some trims and additions were made during the quarter. There were no outright sales or additions of holdings.

The QSV Quality Value Midcap Strategy returned -12.94% and -13.16%, gross and net of fees, for the quarter, leading both the Russell Mid Cap Value Index return of -14.68% and the Russell Mid Cap Index return of -16.85%. QSV’s security selection added value in the Industrial and Financials sectors, while an underweight and negative security selection in Energy and an absence of Utilities companies detracted. QSV generally finds few businesses with high returns on invested capital in the Energy and Utilities sectors and these exposures are typical for our portfolios.

Quality Value Midcap Top Contributors

W.R. Berkley Corporation (WRB) rose during the quarter adding to strong business and stock performance in the first quarter of 2022. WRB provides specialty coverages within the property and casualty insurance and reinsurance markets. Rate increase tailwinds and robust premium growth have supported strong business performance that is reflected in returns on average tangible equity of 18%. While we have conviction in WRB as a business, QSV exited its position during the quarter to capture gains and pursue companies with more compelling valuations.

Shares of Campbell Soup Company (CPB) aided performance during the quarter on strong business performance and an increase in guidance for 2022. Inflation and increasing input costs stand as a risk and management has acknowledged the headwinds that costs for steel cans and other inputs will create in the second half of 2022. Pricing actions in both the first and second half of the year and supply chain productivity gains are expected to offset much of these pressures. CPB produces returns on invested capital of 12% and shares currently trade at a discount to QSV’s estimate of intrinsic value.

Quality Value Midcap Top Detractors

Energy services company Core Laboratories (CLB) was the leading detractor from performance and is discussed above.

As with other bank financials during the quarter, Synovus Financial Corporation (SNV) shares fell sharply. QSV has conviction in SNV and likes the growth potential in its southeastern U.S. footprint. Mortgage loan growth may be depressed by higher interest rates and wealth management revenues will likely be reduced by the depressed market, but higher interest rates and operating efficiencies, that include a reduction in the branch network and greater digital delivery, should more than offset those challenges. SNV produces returns on average tangible equity of 18% and shares are discounted relative to QSV estimate of intrinsic value.

Quality Value Midcap Portfolio Activity

QSV exited CBOE Global Markets (CBOE), Fair Isaac Corporation (FICO), Steve Madden Ltd. (SHOO) and W.R. Berkley (WRB) during the quarter. QSV took advantage of the weakness in consumer stocks with new positions in on-line retailer Etsy Inc. (ETSY) and off-price retailer Ross Stores Inc. (ROST). New positions were also initiated in landscaping equipment provider The Toro Company (TTC) and specialty chemical company Celanese Corporation (CE).

The QSV Select Value Strategy returned -9.72% and -9.91%, gross and net of fees, leading the returns of -15.39% and -16.98% for the Russell 2500 Value and Russell 2500 Indexes, respectively. Select Value is a high conviction strategy that takes QSV’s “best ideas” from our Quality Value Smallcap and Quality Value Midcap strategies. Security selection delivered nearly all the outperformance during the quarter, with the greatest benefit in Industrials and Consumer Discretionary companies. As with QSV’s small and mid-cap portfolios, an underweight and negative security selection in Energy and an absence of Utilities companies detracted.

Select Value Top Contributors

Record high sales lifted the shares of automotive parts provider Dorman Products, Inc. (DORM) during the quarter. Products from DORM are offered through aftermarket retailers such as Advance Auto Parts, AutoZone, and O’Reilly Automotive and distributors such as NAPA. The aging of cars is a tailwind to growth for DORM and the company produces returns on invested capital of 13% while shares remain discounted relative to QSV’S view of intrinsic value.

WD-40 Company (WDFC) shares aided performance during the quarter. The company reported a quarterly upside earnings surprise, while cutting its fiscal year 2022 earnings outlook due to higher oil- based input costs. WDFC benefits from one of the strongest consumer brands with 95% recognition. Growth opportunities are seen in international markets which the company estimates could reach $1 billion. WDFC produces returns on invested capital of 25%.

Select Value Top Detractors

As in the Quality Value Midcap strategy, energy services company Core Laboratories (CLB) was the leading detractor from performance and is discussed above.

Tyler Technologies (TYL) detracted from performance during the quarter but remain a high conviction holding. TYL is the largest provider of enterprise software products focused solely on the public sector, with a focus on local governments where high switching costs stand as Tyler’s competitive advantage. The company has a 98% customer retention rate and incremental margins in its subscription business of over 70%. We believe TYL will benefit from increased government spending on infrastructure, the move of those clients to cloud-based solutions and a shift from the sale of licenses to a software as a service model with its customer base. The company produces returns on invested capital of 11%.

Select Value Portfolio Activity

Keeping with its approach to invest in the best ideas of QSV’s Quality Value Smallcap and Midcap strategies, QSV exited positions in Copart (CPRT), Fair Isaac Corporation (FICO), and Icon PLC (ICLR). QSV initiated positions in Medpace Holdings, Inc. (MEDP), a leading clinical contract research organization, insurance and investment products provider Primerica, Inc. (PRI), and The Toro Company (TTC) during the quarter.

Our Focus on the Long Term

At the risk of restating our comments from the prior quarters, inflation, the Fed’s tightening cycle, slowing economic growth and geopolitical concerns all persist as risks for the remainder of 2022. We add to those risks the possibility of a recession as the Federal Reserve seems committed to its war on inflation while armed with the blunt tool of raising rates. Earnings estimates remain high, but inflationary pressures from input costs and wage increases will present challenges, as may weaker spending by consumers and businesses.

Positives sometimes come in unattractive packaging: While economic contraction is painful, a slow or no growth economy could prompt the Fed to slow the increases in interest rates, offering a boost to stock multiples. The pain felt by investors in the first half of 2022 has cut the valuations of many quality businesses to more attractive levels, offering investors the opportunity to upgrade their holdings. These quality businesses generally have less debt, consistent revenue growth, greater free cash flows, and histories of profitability, all supported by durable competitive advantages. QSV seeks out these qualities in its portfolio companies and we are optimistic that we can deliver compelling long-term results for our clients and ourselves as we invest alongside them.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors (BEM). Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the BQV Midcap Strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the BQV Smallcap Strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Select Value Strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the BEM products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the BEM Products. Lastly, BEM may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequityinvestors.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Lessons Learned in 25 Years of Investing Together

QSV_Lessons Learned in 25 Years

QSV Equity Investors was founded in 2016 as an independent, employee-owned advisory firm by Jeff Kautz and Randy Hughes. Jeff and Randy began investing together twenty-five years ago at Perkins Investment Management, where their boss and mentor, Bob Perkins, first hired Randy in 1995 and then Jeff in 1997. The business and their careers grew. From assisting Bob in the management of a $30 million small cap value fund the late 1990s to responsibilities on multiple value products and over $20 billion in assets by 2016, Jeff became CEO and Chief Investment Officer of the firm and Randy held the roles of Director of Research and Analytics and Equity Analyst. Jeff also served as co-manager of the Janus Henderson Mid Cap Value Fund and the Janus Henderson Value Plus Income Fund.

Twenty-five years into their partnership, Randy and Jeff remain value investors and lessons have been learned over that period. The tools used, and the approach taken to investing clients’ assets have evolved, with the philosophy that investing is a craft where you can learn and get better over time. Seven key lessons, our reflections, and what we believe are the benefits to our clients, follow.

CHEAP IS NOT ENOUGH; QUALITY BOUGHT AT A REASONABLE PRICE ADDS VALUE

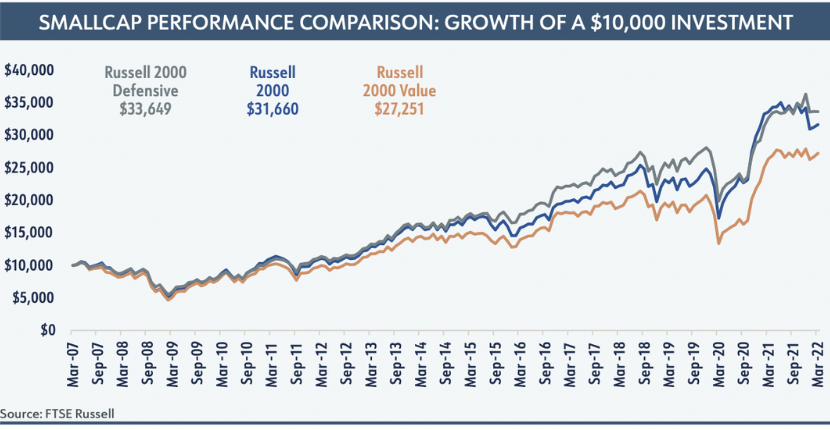

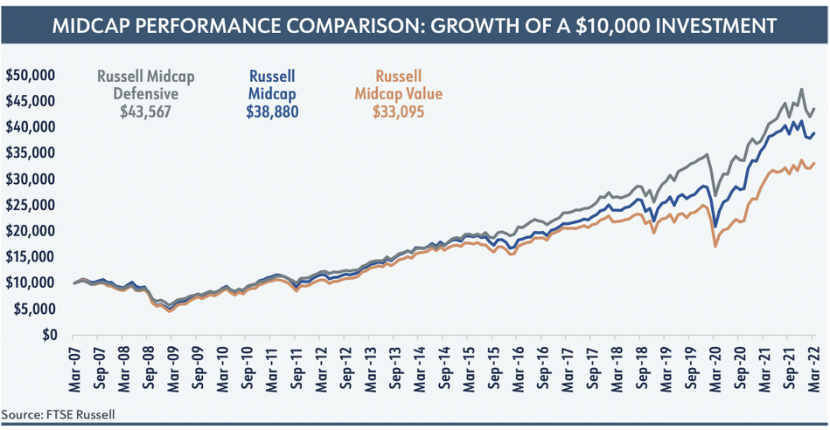

Early in their careers at Perkins, Jeff and Randy focused on cheap stocks, using the 52-week lows list as the starting point for their investment process. Subsequent process steps dug into the fundamentals of each company and an assessment of the durability of its business model. As they gained experience, Jeff and Randy gained conviction in the critical importance of quality and the durable competitive advantages that certain companies earned through successful execution. Their conviction was supported by the “smoother ride” that companies with the characteristics of quality, including strong balance sheets, persistent returns on invested capital, strong and growing free cash flows, and lower levels of debt, delivered. Performance of the Russell Defensive Small and Mid-Cap indexes relative to the Russell value indexes supports this over the last fifteen years as shown on the next page.

Much like the qualities sought by QSV, the Russell Defensive indexes emphasize stocks that exhibit a combination of high return-on-assets, low debt-to-equity, low earnings variability, and low long- and short-term total return volatility. QSV starts its investment process with a singular focus on quality, using both quantitative and qualitative tools to assess the durability of prospective holdings. This focus is grounded in the understanding that we are owners of each business, not traders in its stock.

ALL VALUATION TOOLS ARE NOT EQUAL

Over the course of our twenty-five years of working together, Jeff and Randy have used many methods of valuation. While some can be more useful than others, they have found that these conventional tools are insufficient to meet the needs of the modern investor.

Valuation multiples are the most widely used measures for valuing equities because they are simple to use. These multiples require only two inputs – an estimate of the firm’s value in the numerator and a measure of some valuation metric in the denominator. For example, the trailing 12-month price-to-earnings multiple simply divides a stock’s current share price by the last year’s earnings per share. The simplicity of this type of value calculation also speaks to its shortcomings – multiples tend only to provide high-level snapshots of valuation at a point in time. These shortcomings can misguide investors; a P/E may appear low because the company is at peak earnings. Or, without considering what may happen to the “E,” or earnings, in such a simple equation, investors often can step into value traps – stocks that are cheap for good reason – when relying on multiples.

Another common method of valuation is the Enterprise Value formula, which is used to represent a business’ book value, or the total cost of acquiring that business today. The cost of acquisition can be calculated by adding the total market value of the company’s equity to the total debt that it carries. The resulting sum is a shorthand (though widely accessible) figure that, like multiples, does little to inform us of a business’ investment-worthiness.

Discounted cash flow analysis provides a more accurate measure of the intrinsic value of a business by considering the present value of the cash flows the company is expected to generate in the future and discounting them to arrive at a current, present value. DCF calculates a company’s intrinsic value based on cash flow projections far into the future, which are discounted back to a present value using a combination of a risk-free rate and an equity risk premium. Predicting cash flows is tricky – they are likely to change in time – but a company is not as likely to try to distort cash flows the way it may do with earnings. And applying this cash flow analysis to more predictable, quality businesses is more prone to good outcomes than when assessing more volatile or cyclical businesses.

We lean on QSV proprietary, and more sophisticated, valuation model to identify winning companies. Our Economic Profits Model enables us to take a closer look at what a prospective firm has going on under the hood. Economic Profits and Cash Flow Models are similar and should arrive at the same intrinsic value for a company. However, we believe the Economic Profits Model, which considers both the cost of debt, as DCF does, as well as the cost of equity, provides additional insight. By studying the firm’s capital structure and allocation decisions, such as its debt levels, tax rates, share repurchases and dividend payouts, QSV can assess whether management’s capital allocation decisions are creating or destroying value, making this model a more comprehensive tool for valuing a firm’s stock.

RISK MEANS DIFFERENT THINGS TO DIFFERENT INVESTORS

Allocators today consider many measures of “risk” when weighing the results of QSV and its peer investors. Statistics including standard deviation of returns, downside deviation, drawdown and tracking error relative to an index are among the tools used and, while helpful, are all backward looking in their measurement, using data that is in the past. QSV considers the fundamentals of each prospective investment (using backward looking data) and then considers the prospects of that business looking forward, concentrating our ownership on what we believe will be the best wealth creating holdings for our clients. As owners of a portfolio of quality businesses and as fiduciaries to our clients, QSV views risk as the permanent loss of capital. Our insistence on quality businesses leads to another benefit, albeit a residual of our process; QSV portfolios consistently have lower standard deviations of returns than their indexes.

INDEXES ARE NECESSARY TOOLS, BUT POOR MASTERS

“What gets measured gets done” is a popular saying used to emphasize the importance of performance measurement in business and the business of investment management is no different. Investment indexes are the industry’s tools to benchmark the results of each portfolio over time and, like popular risk measurement statistics, QSV sees these as a necessary tool for our clients and their advisors. We do not manage portfolios with an eye toward adhering to the sector weights or holdings of the relevant index, however, but build portfolios one business at a time. Relative to value indexes and many of our value peers, this generally results in greater exposures to segments of the economy such as healthcare, technology, and consumer staples businesses, where we find quality businesses that possess durable competitive advantages or “moats.” QSV finds fewer of these businesses and has lower weights relative to the indexes in the energy, materials, and financial sectors. Understandably, this results in performance of the portfolios that may be quite different than the indexes in short term periods. QSV always counsels clients to expect this, but we believe we can deliver performance greater than both the value and core indexes over full market cycles, with less risk.

PATIENCE AND CAREER RISK DO NOT LIVE WELL TOGETHER

Delivering excess performance, or alpha, is challenging and even the most skilled investors will have periods, sometimes extended periods, of underperformance. Clients, their advisors, and, as a result, large, publicly-traded investment houses, routinely measure the results of their portfolios against relatively short one- and three-year periods. This is a reality of the business but creates risks to the employment status of many investment professionals. An independent, employee-owned firm must answer to these same client demands but can structure employment and compensation programs to reflect the longer periods of time that may be needed to demonstrate the merits of an investment strategy. At QSV, we believe the correct way to assess the success of a portfolio manager is over a full market cycle, including both peaks and troughs.

CLIENT FIT IS LIKE MARRIAGE

Just as it is difficult to deliver outperformance in active management, it can be hard for asset owners to hold actively managed portfolios, given the disconnects between managers and their respective indexes and periods of underperformance. Just as in a marriage, humility, patience, time, honesty, trust, and communication are all necessary for a successful relationship between a client and its investment managers. QSV is judicious in setting client expectations early in each relationship. We strive to communicate openly and often, and take ownership of our results, both good and bad. Our intention is to have long, trusting relationships with clients who can invest alongside us and benefit from our work.

CULTURE MATTERS

Culture is critical to the success of a business where the assets – human capital – walk out the door every evening. QSV’s team members have worked in small, independent firms and in large publicly traded businesses. We have learned that maintaining the cultural traits that support delivering results for our clients and retaining motivated employees is best done in an independent, employee-owned firm. Traits we hold as critical are:

- Ownership of our defined, repeatable approach to investing.

- Team members sharing a passion for research, investing and client service.

- An ego-free culture that combines diverse, independent thought with collaborative decision-making.

- An emphasis on investment excellence over asset gathering.

- Employee ownership and a willingness to share ownership with key contributors.

CONCLUSION

Lessons learned are often the result of mistakes made and in twenty-five years of investing together Randy and Jeff have made their share. Admitting to those errors, learning, and making the adjustments necessary to QSV’s investment process over time is what will enable us to add value for our clients going forward. The investment world has changed immensely in twenty-five years, with the availability of more information facilitated by rapidly changing technology, changes in investors’ preferences, and with more competition from active and passively managed investment vehicles. QSV’s emphasis on owning quality businesses that create wealth for clients persists, while our process for finding the best of those companies at compelling valuations continues to be refined. We are reminded of the advice of baseball manager Jimmy Dugan in A League of Their Own: “Of course it’s hard. It’s supposed to be hard. If it were easy, everybody would do it. Hard is what makes it great.” We will continue to do the hard work, learn from our mistakes, and refine our craft as we serve our clients.

“Of course it’s hard. It’s supposed to be hard. If it were easy, everybody would do it. Hard is what makes it great.”

ABOUT QSV EQUITY INVESTORS, LLC

QSV Equity Investors, LLC is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Perkins Investment Management and have invested together for over 20 years. For more details on the specific performance and characteristics of QSV’s strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@ballastequity.com.

QSV Equity Investors Awarded Top Guns Designation by Informa Financial Intelligence

Oakbrook, IL – May 24, 2022 – QSV Equity Investors has been awarded multiple PSN Top Guns

distinctions by Informa Financial Intelligence’s PSN manager database, North America’s longest running

database of investment managers. QSV was honored with 6 Star, 5 Star and 4 Star Top Gun ratings for

its Quality Value Midcap strategy in the Mid Value Universe for Q1 2022, highlighting risk-adjusted results

over the trailing three- and five-year periods.

“Volatile markets are currently a fact of life,” noted QSV co-founder and Chief Investment Officer Randy

Hughes. “Ongoing Top Guns recognition by Informa Financial Intelligence is gratifying, as it highlights the

competitive risk-adjusted returns that QSV has delivered for our clients.”

Through a combination of Informa Financial Intelligence’s proprietary performance screens, *PSN Top Guns

(*free registration to view Top Guns) ranks products in six proprietary categories in over 50 universes. This

is a well-respected quarterly ranking and is widely used by institutional asset managers and investors.

Informa Financial Intelligence is part of Informa PLC, a leading provider of critical decision-making solutions

and custom services to financial institutions.

Quality Value Midcap received the 4 Star rating, which is awarded to strategies with an r-squared of 0.80

or greater relative to the style benchmark for the recent five-year period. Moreover, the strategy’s returns

must exceed the style benchmark for the three latest three-year rolling periods. The top ten returns for the

latest three-year period then become the 4 Star Top Guns. The Quality Value Midcap strategy received 5

Star recognition, awarded to those strategies that had an r-squared of 0.80 or greater relative to the style

benchmark for the recent five-year period. Additionally, the strategy’s returns must have exceeded the

style benchmark for the three latest three-year rolling periods. Products are then selected which have a

standard deviation for the five-year period equal or less than the median standard deviation for the peer

group. The top ten returns for the latest three-year period then become the 5 Star Top Guns. Lastly, the

Quality Value Midcap strategy received the 6 Star rating. To attain this rating, the strategy had an r-squared

of 0.80 or greater relative to the style benchmark for the recent five-year period. Moreover, the strategy’s

returns exceeded the style benchmark for the three latest three-year rolling periods. Products are then

selected which have a standard deviation for the five-year period equal or less than the median standard

deviation for the peer group. The top ten information ratios for the latest five-year period then become

the 6 Star Top Guns.

QSV manages three fundamental strategies, Quality Value Midcap, Select Value, and Quality Value

Smallcap, all of which seek to reward clients with performance that is above their benchmarks and peers

over a full market cycle with less volatility. QSV’s investment team invests alongside its clients in small

and mid-cap businesses they believe can sustain high returns on invested capital through durable

competitive advantages. Markets currently present investors with elevated levels of risk and QSV

believes that selectively owning durable businesses purchased at reasonable valuations will be key to

preserving and growing wealth.

“Congratulations to QSV Equity Investors for being recognized as a PSN Top Gun,” said Ryan Nauman,

Market Strategist at Informa Financial Intelligence’s Zephyr. “This highly esteemed designation allows us to

recognize success, excellence and performance of leading investment managers each quarter.”

The complete list of PSN Top Guns and an overview of the methodology can be found on

https://psn.fi.informais.com/

For more details on the methodology behind the PSN Top Guns Rankings or to purchase PSN Top Guns

Reports, contact Margaret Tobiasen at Margaret.tobiasen@informa.com.

For more details on the specific performance and characteristics of QSV’s strategies, including a fully

GIPS compliant presentation, please visit www.qsvequityinvestors.com.

About QSV Equity Investors, LLC

QSV Equity Investors is an employee-owned asset management firm that invests alongside its clients

in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these

portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook

Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who

previously held senior roles at Perkins Investment Management and have invested together for 25 years.

About Informa Financial Intelligence’s Zephyr

Financial Intelligence, part of the Informa Intelligence Division of Informa plc, is a leading provider of

products and services helping financial institutions around the world cut through the noise and take

decisive action. Informa Financial Intelligence’s solutions provide unparalleled insight into market

opportunity, competitive performance and customer segment behavioral patterns and performance

through specialized industry research, intelligence, and insight. IFI’s Zephyr portfolio supports asset

allocation, investment analysis, portfolio construction, and client communications that combine to help

advisors and portfolio managers retain and grow client relationships. For more information about IFI, visit

https://financialintelligence.informa.com. For more information about Zephyr’s PSN Separately Managed

Accounts data, visit https://financialintelligence.informa.com/products-and-services/data-analysis-and-tools/psn-sma.

Media Contact:

Dave Mertens

QSV Equity Investors, LLC

dmertens@ballastequity.com

(630) 376-4392

QSV Equity Investors Q1 2022 Commentary

QSV Equity Investors

Q1 2022 Commentary

More information including since-inception performance for each of the strategies may be found at www.qsvequityinvestors.com.

QSV concluded its commentary last quarter with a list of “known risks” that included a continuation of inflation, the Federal Reserve’s tightening cycle and trajectory, and the fact that attention paid by investors to geopolitical risks stood at a four-year low, while the ambitions of China, Iran and Russia continued to rise. These risks emerged in more profound ways than we expected, with war in Ukraine, a more hawkish Fed, and inflation spiking to 40-year highs. Markets reacted to these risk factors with heightened volatility and negative returns across equity market caps. Performance by energy stocks greatly outstripped all other sectors as worries over global supply – already escalated prior to the war in Ukraine – rose further.

QSV Strategy Quarterly Performance

The QSV Quality Value Smallcap Strategy returned -6.50% and -6.58%, gross and net of fees, lagging the Russell 2000 Value Index return of -2.40% while leading the Russell 2000 Index return of -7.53%. QSV has historically been significantly underweight in Energy holdings, as these businesses generally do not have the high returns on invested capital or consistency of business performance we seek. This created meaningful headwinds to performance, as did robust performance by certain index constituents in the Defense and Shipping industries. Healthcare and Communication Services holdings helped performance, while holdings in the Energy and Industrials sectors detracted.

Quality Value Smallcap Top Contributors

Energy services company Core Laboratories (CLB) rose over 40% as investor sentiment turned favorable toward the company’s prospects in its reservoir description and production enhancement services divisions. CLB is the singular energy holding in the QSV strategy and has competitive advantages that include its intangible assets (patents, proprietary technology, and human capital) and network effects (multi-client reservoir studies). Prior to the start of the conflict in Ukraine, CLB announced that it expects double digit gains in 2022 for both its business segments; these gains could improve further as exploration and production increases.

Shares of on-line automotive sales platform CarGurus, Inc. (CARG) also rose during the quarter. CARG offers a leading marketplace for both individuals and dealerships to buy, market and sell vehicles in the U.S. as well as Canada and the U.K. CARG has a strong network effect competitive advantage with over thirty-nine million unique visitors each month and over 30,000 paying dealerships globally. Positive stock performance was supported by quarterly revenues that exceeded Street expectations by over 20% and by the company’s investment in dealer-matching service CarOffer.

Quality Value Smallcap Top Detractors

Shares of 1-800 Flowers.com (FLWS) fell 45% during the quarter. Challenges to the company’s margins included higher freight, shipping, and labor rates all hitting during its important holiday season. FLWS is working to offset these challenges by adding more automation into its manufacturing and distribution facilities, raising prices where possible, and building additional inventories. FLWS continues to have strong and growing free cash flows and delivers average returns on invested capital of 12%. FLWS has a proven record of making accretive acquisitions, something we expect will continue to boost business performance.

Shares of Watts Water Technologies, Inc. (WTS) fell during the quarter, along with the other housing related companies, despite strong earnings that exceeded expectations. WTS is a global provider of Smart and Connected water conservation, safety, and flow control products. Share price performance was impacted by conservative guidance for the coming year; WTS has tough comparisons to beat for the first two quarters of 2022 and is making growth investments in its business. The company does have pricing power and we expect price increases and the shift to energy efficient products to aid performance in the second half of 2022.

Quality Value Smallcap Portfolio Activity

QSV exited its position in Eagle Pharmaceuticals (EGRX). Prior to the invasion of Ukraine, a new position was initiated in Aerojet Rocketdyne Holdings, Inc. (AJRD), a manufacturer of aerospace and defense products and systems. Also initiated was a position in Medpace Holdings Inc. (MEDP), a leading clinical contract research focused primarily on full-service project work for small- and mid-sized biopharmaceutical clients. AJRD and MEDP each produce high returns on invested capital, 18% and 16% respectively, and each sells at a meaningful discount to QSV estimate of intrinsic value.

The QSV Quality Value Midcap Strategy returned -7.06% and -7.29%, gross and net of fees, for the quarter, lagging the Russell Mid Cap Value Index return of -1.82% and the Russell Mid Cap Index return of -5.68%. QSV security selection added value in the Industrial and Financials sectors, while selection in Healthcare and a meaningful underweight to Energy holdings detracted from strategy performance. QSV has historically been significantly underweight in Energy holdings, as these businesses generally do not have the high returns on invested capital or consistency of business performance we seek.

Quality Value Midcap Top Contributors

Energy services company Core Laboratories (CLB) was the leading contributor to performance and is discussed above.

W.R. Berkley Corporation (WRB) rose over 20% during the quarter as earnings exceeded expectations. WRB provides specialty coverages within the property and casualty insurance and reinsurance markets. The company expects strong business performance to continue, as rate increases in excess of claims trends are anticipated to continue. WRB continues to sell at a significant discount to QSV’s estimate of intrinsic value.

Quality Value Midcap Top Detractors

Masimo Corporation (MASI) shares fell in mid-quarter on the news of its planned acquisition of consumer technology company Sound United. MASI is a medical technology company which develops, manufactures, and markets non-invasive vital sign monitoring devices. While the thesis behind the acquisition is confusing on the surface, it makes strategic sense as MASI is eager to build infrastructure and relationships for marketing its future consumer-focused products, such as the Masimo W1 smartwatch. MASI produces returns on invested capital of 18% and remains a key portfolio holding. QSV will closely monitor the integration of Sound United along with the overall business performance of the company.

Icon PLC (ICLR) shares fell over concerns that business would slow, post COVID, and that it could stumble in its integration of newly acquired PRA Health. ICLR – and PRAH – are clinical research organizations (CROs) providing outsourced development services to the pharmaceutical, biotechnology, and medical device industries. ICLR has a history of being conservative as it communicates its outlook and previously communicated its expectations for 2022. The cultures of ICLR and PRA Health are similar, and the combined organization will bring synergies and benefit from reduced client concentrations.

Quality Value Midcap Portfolio Activity

QSV exited Amdocs Limited (DOX), Maximus Inc. (MMS), and Qualys Inc. (QLYS) during the quarter. New positions were initiated in EPAM Systems Inc. (EPAM), a provider of software and digital platform engineering services, global freight forwarding company Expeditors International of Washington (EXPD), and Helen of Troy Ltd. (HELE), a consumer products company with brands including Braun, Hydro Flask and Revlon.

The QSV Select Value Strategy returned -8.76% and -8.96%, gross and net of fees, trailing the returns of -1.50% and -5.82% for the Russell 2500 Value and Russell 2500 Indexes, respectively. Select Value is a high conviction strategy that takes QSV’s “best ideas” from its Quality Value Smallcap and Quality Value Midcap strategies. Security selection more than offset the negative impact of an overweight in Technology companies during the quarter. QSV’s overweight and its security selection detracted from performance in Healthcare and its meaningful underweight to Energy also detracted.

Select Value Top Contributors

Energy services company Core Laboratories (CLB) was the leading contributor to performance and is discussed above.

Financial technology company Jack Henry & Associates, Inc. (JKHY) was the second greatest contributor to performance during the quarter. JKHY provides automation software, payment processing, and outsourcing solutions to community banks and credit unions and has moved up market into larger banking organizations over the past ten years. The company produces returns on invested capital of 20%, supported by high switching costs and a scalable business model.

Select Value Top Detractors

As in the Quality Value Midcap strategy, holdings Masimo Corporation (MASI) and Icon PLC (ICLR) were the greatest detractors. Comments on each are noted above.

Select Value Portfolio Activity

Adhering to QSV’s emphasis on owning its best small and mid-cap ideas within the Select Value portfolio, QSV exited Amdocs Limited (DOX), Maximus Inc. (MMS), and Qualys Inc. (QLYS) during the quarter. New positions were entered in Clorox (CLX), an existing holding in the QSV Quality Value Midcap strategy, and Helen of Troy Ltd. (HELE).

Our Focus on the Long Term

With today’s “perfect storm” of risk factors, the near-term outlook is more cloudy than usual. Inflation, the Fed’s tightening cycle, and geopolitical concerns all weigh on the markets and seem likely to persist during 2022. What seems certain is that economic growth will be slower, leading to slowing corporate earnings growth. The earnings cycle and earnings growth, company by company, will be in focus, favoring stable and profitable quality businesses such as those emphasized in the QSV strategies.

QSV advises clients that investing in high quality businesses is a winning strategy over time, but we know there will be periods of underperformance. The first quarter of 2022 was painfully such a time, as energy and companies tied to commodity prices drove returns, while stable companies with high returns on invested capital lagged significantly. Investors who can accept these near-term “disconnects” with benchmarks and have the patience to commit to long term ownership are rewarded over time with higher returns and less volatility. We continue to stay true to our investment process and seek out quality businesses that can be “price makers” in these challenging times.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors (BEM). Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the BQV Midcap Strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the BQV Smallcap Strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Select Value Strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the BEM products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the BEM Products. Lastly, BEM may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To receive a GIPS report, please contact QSV at (844) 3-BALLAST.

CSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

War, the Markets, and the Case for Quality February 25, 2022

QSV Equity Investors

February 25, 2022

More information including since-inception performance for each QSV strategy may be found at www.qsvequityinvestors.com.

War

Markets have been bracing for conflict between Russia and Ukraine for much of 2022 and, on Thursday, this conflict became a reality. President Vladimir Putin has stated that Ukraine “is an inalienable part of [Russia’s] history, culture, and spiritual space” and seems intent on restoring what was the U.S.S.R. Equity markets reacted with wild swings, including a near seven hundred basis point trough to peak move by the NASDAQ. The initial “risk off” reaction triggered by news of Russia’s invasion was followed by a sharp rally as investors seemed relieved by sanctions that were less severe than feared and the possibility that the Federal Reserve’s expected rate hikes be muted as it wishes to avoid economic slowdown.

The Markets

Oil and natural gas prices have been on the rise in 2022 and the conflict between Russia and Ukraine sent them higher. Prices have been driven by the recovery in global demand and the discipline shown by OPEC in sticking to its promise to slash oil production. Further, there has been a low level of investment in hydrocarbon production in recent years as energy companies have instead returned capital to shareholders. Shares of oil and natural gas exploration and production companies, including Marathon Oil, Halliburton, Hess, and Occidental Petroleum, have been propelled by these rising prices and have been the bright spots in small and mid-cap indexes during an otherwise negative 2022. Through Thursday, for example, the Energy sector was up over 19% in the Russell Mid Cap Value index while the benchmark, itself, was down 7%. Similarly, the Energy sector was up over 15% year-to-date in the Russell 2000 Value index and the benchmark was down nearly 7%.

The Case for Quality

Fears over rising inflation, the persistence of COVID, and concerns over the pace of rate hikes by the Federal Reserve were all worries for investors entering 2022. The war between Russia and Ukraine only adds to these, with uncertainty around additional sanctions, the duration of the conflict and added inflationary pressures from energy and agricultural inputs. The resulting volatility is a reminder that risk goes hand in hand with the pursuit of rewards in investing and, in our view, makes the case for long term ownership of quality businesses. Quality businesses, in QSV’s definition, deliver high returns on invested capital supported by durable competitive advantages. These companies share strong balance sheets, lower debt and pricing power, all characteristics that offer stability in volatile times. Businesses like Clorox, Campbell Soup, and McCormick & Company offer essential products and services and possess scale advantages and intangible assets that give them staying power and result in a “smoother ride” for investors in their shares. Equity investing is essential as retirement plans provide benefits to plan participants, foundations strive to fulfill their missions and families build secure futures. Allocations to quality businesses have proven to offer strong long-term results with less volatility in turbulent times.

Disclaimer:

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To receive a GIPS report, please contact QSV at (844) 3-BALLAST.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

QSV Equity Investors Q4 2021 Commentary

QSV Equity Investors

Q4 2021 Commentary

More information including a since-inception performance for each of the strategies may be found at www.qsvequityinvestors.com.

Equity markets marched higher in the quarter, with returns in large capitalization indexes outpacing those of small cap indexes. Businesses and investors faced numerous challenges – research firm Sentieo cited “supply chain,” “inflation” and “variant” as the most mentioned words on Wall Street calls – but returns were lifted by an ongoing combination of favorable monetary policy and fiscal stimulus which has fueled earnings growth into the second year of economic recovery. Investors have been slowly moving away from the higher beta and long duration stocks that led the market since the 2020 lows to lower beta, higher quality defensive stocks more recently. Using the Russell Stability indexes as proxies for high and low quality, the Russell Defensive indexes containing businesses with higher Returns on Assets, lower leverage, and lower volatility meaningfully outperformed lower-quality businesses, as measured by the Russell Dynamic indexes, across the market cap spectrum.

QSV Strategy Quarterly Performance

The QSV Quality Value Smallcap Strategy returned 6.67% and 6.57% gross and net of fees, beating both the Russell 2000 Value and Russell 2000 Indexes’ returns of 4.36% and 2.14%, respectively. Quality “QSV-like” businesses, those with less sensitivity to economic and credit cycles and with more sustainable business models, outperformed. Active returns were greatest in the Healthcare, Communication Services, and Financials sectors, while Utilities and Cash detracted from performance. Security selection was a strong contributor to performance, with the most impactful contributions in Healthcare and Real Estate companies.

Quality Value Smallcap Top Contributors

Forward Air (FWRD) rose over 45% during the quarter as the company continues to grow organically and through acquisitions. FWRD is the leader in the deferred airfreight transportation market, where it provides time-sensitive ground transportation (airport-to-airport) to other transportation providers such as freight forwarders and airlines. The mix of FWRD’s business is shifting to higher margin, less labor-intensive palletized cargo which bodes well for an improvement in its already strong 12% return on invested capital.

National Storage Affiliates Trust (NSA) shares rose during the quarter as occupancy rates and pricing power remained high. The company continues to grow through acquisition, focusing on secondary markets where there is less competition for properties and where the company believes there is less sensitivity to economic fluctuations. NSA raised its dividend for the third consecutive quarter in November while maintaining a conservative payout ratio.

Quality Value Smallcap Top Detractors

Although PaySign (PAYS) beat revenue estimates for the quarter and raised the bottom end of its guidance for full year EBITDA, shares fell significantly during the quarter. The business performance continued to be impaired because of the impact of the COVID pandemic on the company’s plasma business. PAYS also cited pandemic-related government stimulus programs as disincentives for individuals to donate plasma. QSV exited its position in PAYS in favor of better ideas.

As with many retail and e-commerce stocks, shares of 1-800 Flowers.com (FLWS) fell sharply during the quarter. Headwinds to the company’s results include supply chain issues, including rising shipping and container costs, and higher labor rates. FLWS is working to offset some of these challenges with price increases and greater automation. The company has also made accretive acquisitions, including a seller of premium seafood and organic foods, Vital Choice, which offers synergies with existing holding Harry & David. FLWS continues to have strong average returns on invested capital of 12% and continues to be a holding for QSV.

Quality Value Smallcap Portfolio Activity

QSV exited positions in Physicians Realty Trust (DOC), Dril-Quip Inc. (DRQ), InterDigital Inc. (IDCC), MGE Energy, Inc. (MGEE), PaySign Inc., (PAYS), and Zynex Inc., (ZYXI). Zix Corporation (ZIXI) was excited as it was acquired by OpenText, a provider of information management solutions. QSV entered new positions in Frontdoor Inc. (FTDR), a provider of tech-enabled home services and warranties, and Getty Realty Corp. (GTY), owner of a convenience store and gasoline station properties that operate under brands including BP, Citgo, Exxon, and Shell. Also added were Postal Realty Trust (PSTL), the only publicly traded REIT focused on the management of properties leased to the U.S. Postal Service, and Progress Software Corp. (PRGS), a provider of cloud-based security solutions.

The QSV Quality Value Midcap Strategy returned 10.65% and 10.38%, gross and net of fees, for the quarter, leading both the Russell Mid Cap Value Index return of 8.54% and the Russell Mid Cap Index return of 6.44%. QSV added value in the Consumer Discretionary and Healthcare sectors, while Energy and Utilities exposures detracted from strategy performance. Security selection delivered an excess performance in 7 of 11 S&P sectors, with selection in Healthcare and Consumer Discretionary companies delivering the most meaningful returns.

Quality Value Midcap Top Contributors

Extra Space Storage Inc. (EXR) was the second largest contributor to performance during the quarter. EXR controls the second largest self-storage portfolio in the United States. Its scale advantage and the data that is derived from its portfolio allows EXR to move swiftly when adjusting pricing to reflect changing market trends. High occupancy rates and acquisitions supported robust performance during the quarter.

Swimming pool supplies provider Pool Corp (POOL) was the greatest contributor to performance during the quarter. The stay-at-home environment buoyed sales of Pool’s products and its share price. While the expected sales in new residential pools have slowed from strong pandemic growth, these represent less than 20% of sales for the company and its installed base will continue to deliver strong results, in our view. POOL has average returns on invested capital of 27% and continues to be a holding for QSV.

Quality Value Midcap Top Detractors

Core Laboratories (CLB) was the leading detractor from performance as COVID-19 related disruptions, hurricanes in the Gulf Coast, and supply chain issues impacted its business performance. CLB is the leader in providing core and reservoir analysis to oil and gas companies. Competitive advantages include its intangible assets (patents, proprietary technology, and human capital) and network effects (multi-client reservoir studies). The company anticipates growing customer demand in both the U.S. and international markets in 2022 and has increased raw materials inventories to address its supply chain challenges. CLB is one of the more profitable names in the group and continues to be a holding.

Despite quarterly performance that met expectations and raising the company’s guidance for the full year, Fleetcor Technologies Inc. (FLT) detracted from performance during the quarter. FLT is a provider of global business payment processing solutions, processing more than 1.6 billion transactions each year in segments that include trucking, lodging, toll roads and corporate payments. Its scale in these segments and the growth in business-to-business payments serve as strong moats for the business. Supply chain bottlenecks and driver shortages have impacted trucking within its fuel payments segment, but we see these as short-term issues and have conviction in the business.

Quality Value Midcap Portfolio Activity

QSV exited Physicians Realty Trust (DOC), MGE Energy, Inc. (MGEE), MSCI Inc. (MSCI), and Waste Connections (WCN), during the quarter. Aspen Technology (AZPN) was exited as it entered into a definitive agreement to be acquired by Emerson Electric, a global technology and engineering company. New positions were initiated in consumer products company Church & Dwight (CHD), the well-known provider of cleaning and disinfecting products company Clorox (CLX), food and snack company Campbell Soup (CPB), and video game publisher Take-Two Interactive Software, Inc. (TTWO).

The QSV Select Value Strategy returned 9.44% and 9.20%, gross and net of fees, leading the returns of 6.36% and 3.82% for the Russell 2500 Value and Russell 2500 Indexes, respectively. Select Value is a high conviction strategy that takes WSV “best ideas” from its Quality Value Smallcap and Quality Value Midcap strategies. Exposures in the Healthcare and Consumer Discretionary sectors aided returns, while the Industrials and Energy sectors detracted. Security selection can be credited for all the outperformance for the quarter, with Healthcare, Consumer Staples and Information Technology holdings most notably contributing.

Select Value Top Contributors

National Storage Affiliates Trust (NSA) was the leading contributor to performance during the quarter. Its results are noted above.

Pool Corp (POOL) was the second greatest contributor to performance during the quarter. Its results are discussed above.

Select Value Top Detractors

Core Laboratories (CLB) was the leading detractor from performance in the Select Value strategy and is discussed above.

Fleetcor Technologies Inc. (FLT) was the second largest detractor from performance during the quarter and is also addressed above.

Select Value Portfolio Activity

Adhering to QSV’s emphasis on owning its best small and mid-cap ideas within the Select Value portfolio, new positions were initiated in Church & Dwight (CHD), Getty Realty Trust (GTY), and Take-Two Interactive Software (TTWO). QSV exited its holdings in Aspen Technology (AZPN), MSCI (MSCI), and Waste Connections (WCN).

Our Focus on the Long Term

For much of 2021, the markets rose seemingly without concern for potential risks. QSV sees the New Year through the lens of opportunity, but with a keen eye on risk management through ownership of quality businesses. Known risks include:

- A continuation of inflation and its effects on consumers’ purchasing power and the pricing power of businesses.

- COVID, and global responses to the pandemic, persist as risks.

- Actions by the Federal Reserve that may progress at levels greater or lesser than anticipated.

- The fact that attention paid by investors to geopolitical risks stands at a four-year low, according to BlackRock, while the ambitions of China, Iran and Russia continue to rise. Our own political landscape in the U.S. that remains highly polarized.

The potential impact of each of these is important for investors to consider, yet the macro future is not knowable. We do know that rising rates will impact the valuations of equities, particular higher growth names heavily reliant on future earnings. We also know that lower quality value stocks had their day in the sun in 2020 and early 2021 after briefly being left for dead at the start of the pandemic. QSV believes that our area of focus – quality businesses with durable competitive advantages, strong balance sheets and strong cash flow generation – will serve investors particularly well in the coming year and beyond. These businesses, purchased at reasonable valuations, have a long history of providing solid participation in rising markets and shock absorption for the surprises that come.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors (BEM). Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the BQV Midcap Strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the BQV Smallcap Strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Select Value Strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the BEM products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the BEM Products. Lastly, BEM may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To receive a GIPS report, please contact QSV at (844) 3-BALLAST.