Category: Commentary

Q3 2024 Commentary

Q3 2024 Commentary

Last quarter we lamented that investors have paid little attention to the pond QSV fishes in, small and mid-cap stocks. After considerable waiting, small and mid-cap stocks outperformed the stocks of their larger brethren in Q3 2024, although it was hardly a straight line up and to the right during the quarter. Smaller companies’ stocks began a rally in July that was punctuated by selloffs in early August and early September. Their climb persisted higher to the end of the quarter supported by an interest rate cut by the Federal Reserve and investor confidence that inflation was under control. QSV participated well during the quarter, with our Small Cap and Select strategies outperforming their respective benchmarks while our Mid Cap lagged its index.

More information including since-inception performance for each QSV strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned 10.30% and 10.21%, gross and net of fees, respectively, leading the Russell 2000 Value Index return of 10.15% and the Russell 2000 Index return of 9.27%. An underweight to Energy companies aided performance. Security selection and an overweight in Industrials also helped performance. Security selection and an overweight to Technology businesses detracted from returns.

QSV Small Cap Top Contributors

Doximity, Inc. (DOCS) shares rose over 55% supported by strong revenue and earnings, both of which surpassed analysts’ expectations. DOCS also provided optimistic Q2 and fiscal year 2025 guidance, projecting higher revenue than analysts’ expectations. DOCS offers a suite of tools that support an online community for physicians, nurse practitioners and physicians’ assistants, enabling them to coordinate patient care, conduct patient visits and manage their careers, DOCS’ Q1 earnings call highlighted a net revenue retention rate of 114% and 21% growth from its top 20 clients. The company has returns on invested capital of 16%.

Hawkins Inc. (HWKN) rose more than 40%, contributing to performance. HWKN is a leading provider of chemicals and ingredients sold through its industrial, water treatment and health and nutrition segments. The company continues to benefit from capital deployment and fast growth in its largest segment, the high margin water treatment business, which is expected to drive higher earnings and free cash flow growth. HWKN produces returns on invested capital of 13%.

QSV Small Cap Top Detractors

Simulations Plus Inc. (SLP) was the leading detractor from performance for the quarter as shares dropped on a mixed demand environment and lower margins. SLP is a leading provider of software and services used by major pharmaceutical, biotech, and regulatory agencies to make better informed, data-driven decisions. We see the potential for improved demand and long-term value creation due to the company’s high switching costs, intellectual assets, and a 93% renewal rate by its customers. SLP produces operating margins of 26% on average and its shares are well below our estimate of intrinsic value.

Helen of Troy (HELE) shares declined during the quarter as management lowered guidance. The consumer products company owns strong discretionary brands that are organized into its Home & Outdoor and Beauty & Wellness segments. Entering the quarter, we incorrectly believed that lower expectations were priced into the stock. With its additional pullback during the quarter and our belief that its risks are reflected, we added to our position. We like HELE’s strong free cash flows and the restructuring plan that management has instituted to cut costs.

QSV Small Cap Portfolio Activity

Shares of Hancock Whitney Corporation (HWC) were purchased as QSV sought to increase its exposure to Financials ahead of anticipated interest rate cuts. MGP Ingredients (MGPI), a maker of premium distilled spirits and specialty wheat protein and starch food ingredients, was also added as its shares reached an attractive valuation. MGPI was previously a profitable holding of QSV Small Cap and has been steadily monitored by our team.

QSV Mid Cap returned 8.15% and 7.89%, gross and net of fees for the quarter, trailing the 10.08% return of the Russell Mid Cap Value Index and the Russell Mid Cap Index return of 9.21%. Security selection in Technology companies helped performance while an overweight to the sector detracted. Company selection and an overweight to Financials also aided performance. Selection in Industrials and Healthcare companies detracted from performance.

QSV Mid Cap Top Contributors

Shares of Jones Lang LaSalle (JLL) was the leading contributor to performance as shares rose over 31%. Revenues and earnings for JLL both exceeded industry trends and came in above expectations. The outlook for commercial real estate remains challenging but JLL offers a broad array of services, and the company is cautiously optimistic for the remainder of the year. During the quarter, JLL completed its acquisition of SKAE, enhancing its project management capabilities for data centers.

Equity exchange and market-services provider NASDAQ (NDAQ) also contributed to performance during the quarter as its shares rose 21.56%. In June, the company announced its acquisition of Adenza, a provider of risk management and regulatory software for the financial industry. The acquisition strengthens the position of NDAQ within the global financial system and speeds its transition to a greater emphasis on recurring revenue business.

QSV Mid Cap Top Detractors

Independent exploration and production company APA Corporation (APA) was the leading detractor to performance during the quarter as its shares fell 16% as the company reported mixed results. APA produced better-than-expected earnings and total production and reported a return of approximately 60% of free cash flows back to shareholders. However, APA offered production guidance for the coming quarter that was below expectations due to lower demand and anticipated higher capital expenditures.

Contract research organization ICON PLC (ICON) detracted from performance during the quarter as the company reported revenues and earnings that were below expectations. To the positive, the ICON’s backlog increased year over year and it provided earnings guidance that is above previous guidance. Management noted that the biotech sector is facing short-term challenges due to a tightening funding environment and restructuring and budget cuts from large pharma clients. ICON earns returns on invested capital of 8% and its shares are trading at a significant discount to our estimate of its intrinsic value.

QSV Mid Cap Portfolio Activity

QSV added Medpace Holdings Inc. (MEDP), a leading clinical contract research organization (CRO) focused on Phase I-IV clinical development, to its Mid Cap portfolio during the quarter. Other trims and additions to existing positions were made based upon valuation and our convictions in the fundamentals of the businesses.

QSV Select returned 10.72% and 10.45%, gross and net of fees, beating the returns of the Russell 2500 Value and Russell 2500 Indexes of 9.63% and 8.75%, respectively. Select is a high conviction strategy that holds QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection was positive in Industrials. Selection and an overweight in Information Technology and Consumer Discretionary holdings also aided performance. Selection detracted from returns in Financials and Healthcare holdings.

QSV Select Top Contributors

Doximity Inc. (DOX) was the leading contributor to performance during the quarter and is discussed above.

Cohen & Steers Inc. (CNS) rose over 33%, contributing to outperformance during the quarter. The company reported an increase in assets under management in June, attributed to market appreciation, despite net outflows, and reported quarterly earnings and revenues that were above estimates. CNS specializes in liquid real assets such as REITs and offersinstitutional accounts, open-end funds, and closed-end funds. The company has net cash, strong margins and returns on invested capital of 36%, which support a healthy dividend, share buybacks and repayment of debt.

QSV Select Top Detractors

Napco Security Technologies (NSSC) shares fell 21.86% during the quarter on news of slowing growth and insider selling. NSSC is a global provider and manufacturer of high-tech security products, including access control systems, door-locking products, intrusion and fire alarm systems and video surveillance products. The company is focused on doubling revenue within its recurring, high-margin Services business in the next 2-3 years and currently produces returns on invested capital of 18% while selling at a meaningful discount to our measure of intrinsic value.

Clinical contract research organization Medpace Holdings Inc. (MEDP) also detracted from performance as revenues and new bookings were below expectations. We continue to like MEDP because it operates in a large $45b market where its customers often do not have the required development expertise and infrastructure in-house, and the tools and testing are highly scripted in law, regulation, and practice. MEDP exhibits low capital intensity, resulting in ROICs of 25% on average.

QSV Select Portfolio Activity

Limited trading was done in QSV Select during the quarter, with trims and additions made to address valuations and quality upgrades. One new position was initiated in a previous portfolio holding, MGP Ingredients (MGPI), a maker of premium distilled spirits and specialty wheat protein and starch food ingredients.

Our Focus on the Long Term

Most expect interest rate cuts by the Federal Reserve to continue, which should benefit smaller companies that require borrowing and, in many cases, offer better potential growth. Like the two-handed economist, we must consider that “on the other hand” there are cracks in the economy, geopolitical concerns, the Longshoremen’s strike that could spark inflation, and a contentious election cycle to grind through. Valuations continue to be more compelling in small and mid-cap businesses, and the possibility that something negative occurs – a pause in rate cuts, a recession, or some other shock – is priced into these stocks more than those of large companies. Investors should be selective and demand balance sheet strength, high returns on invested capital, and strong free cash flows as a substantial portion of smaller companies continue to be unprofitable. We suspect that year-end asset allocation reviews will reveal an overweight to large caps that have outperformed year to date and for the trailing years and believe the answer is quality small and mid-caps purchased at reasonable prices.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Q2 2024 Commentary

Q2 2024 Commentary

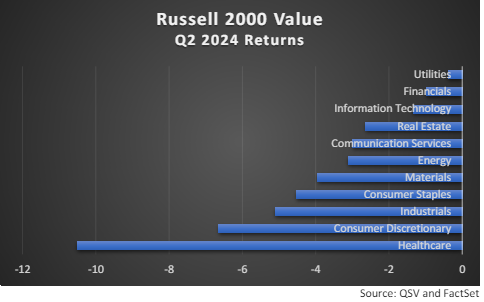

No one needs another investment commentary noting the divergence of Nvidia and the “Magnificent 7” stocks’ performance with that of the broader market, but it is hard to live through a quarter like Q2 2024 without that on our minds. This compact group of companies has contributed more than 60% of the returns of the index in 2024 and, when the returns of the capitalization weighted S&P 500 are compared to an equally weighted S&P 500, there is a 10% difference in favor of the cap weighted benchmark. While this dynamic plays out, investors have paid little attention to the pond QSV fishes in, small and mid-cap equities, where the returns were quite different, and negative during the quarter. Each sector of the Russell 2000 Value index delivered losses in Q2, with Utilities (supported by the prospects for data centers for the AI revolution?) only slightly in negative territory and Healthcare, where QSV finds an ample supply of quality businesses, suffering losses of more than 10%. Returns for mid-cap indexes were in similar,

negative, territory.

More information including since-inception performance for each QSV strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned -3.76% and -3.84%, gross and net of fees, respectively, lagging the Russell 2000 Value Index return of -3.64% and the Russell 2000 Index return of -3.28%. Security selection in Healthcare helped performance, while an overweight in the sector detracted. Selection in Real Estate also aided performance. Selection in Industrials and Financials businesses detracted from returns.

QSV Small Cap Top Contributors

Napco Security Technologies Inc. (NSSC) shares rose nearly 30% supported by strong growth in revenues and gross margins in its business units. NSSC is a global provider and manufacturer of high-tech security products, including access control systems, door-locking products, intrusion and fire alarm systems and video surveillance products. The company is focused on doubling revenue within its recurring, high-margin Services business in the next 2-3 years and currently produces returns on invested capital of 17% while selling at a discount to our measure of intrinsic value.

Hawkins Inc. (HWKN), rose more than 18%, contributing to performance. HWKN is a leading provider of chemicals and ingredients sold through its industrial, water treatment and health and nutrition segments. The company has benefitted from fast growth in its high margin water treatment business which is expected to drive higher earnings and free cash flow growth as it represents a larger portion of the firm’s overall revenues. HWKN produces returns on invested capital of 13%.

QSV Small Cap Top Detractors

Shares of clinical research organization Fortrea Holdings (FTRE) dropped more than 40% during the quarter as the company fell short of analysts’ estimates of revenues and earnings and the company lowered its outlook. The company, spun out of LabCorp (LH) in 2023, benefits from offering tools and testing to the biotechnology and pharmaceutical industries that are highly scripted in law, regulation, and practice. QSV believes that it is not uncommon for a company to struggle initially post-spinoff and has confidence in the long-term outlook for FTRE. As a result, we added to our position on weakness in the share price.

Alamo Group (ALG) shares declined during the quarter as a five-week strike in one of its plants is expected to impact the quarter’s financial results. The manufacturer of agricultural and vegetation maintenance equipment settled the strike with a five-year contract that should remove the risk of labor disruption for some time. ALG operates as forty global brands in two key divisions: industrial equipment and vegetation management equipment. The company benefits from an extensive dealer network and leading market share. Sixty percent of its revenues come from state and municipal government contracts.

QSV Small Cap Portfolio Activity

Shares of Forward Air (FWRD) were sold after the company added debt for its Omni Logistics acquisition and, in our view, could not clearly define the mission for the combined business. PubMatic (PUBM) and Shutterstock (SSTK) were each sold for valuation reasons. Scotts Miracle-Gro (SMG) was sold as they continued to struggle with the exposure to the cannabis industry and the addition of debt, reducing our estimate of the company’s intrinsic value. Proceeds were invested in existing holdings as well as new holding Catalyst Pharmaceuticals(CPRX), a biopharmaceutical company focused on developing therapies for people with rare, debilitating neuromuscular and neurological diseases.

QSV Mid Cap returned -5.15% and -5.38%, gross and net of fees for the quarter, trailing the -3.40% return of the Russell Mid Cap Value Index and the Russell Mid Cap Index return of -3.35%. Security selection in Consumer Staples companies helped performance, as did company selection and an overweight to Information Technology companies. Selection in Financials detracted as did selection and an overweight to Healthcare.

QSV Mid Cap Top Contributors

Monolithic Power SystemsInc. (MPWR) was the leading contributor to performance in the quarter as the company delivered strong earnings growth and benefitted from the outlook for AI-related tailwinds. MPWR is a global provider of high-performance, semiconductor-based power solutions. As a “fabless” company – one that does not manufacture the chips used in its products – MPWR has profited from devoting more resources to chip design rather than capital expenditures, resulting in greater free cash flows, higher margins, and returns on invested capital of 22%.

Teradyne Inc. (TER), a provider of semiconductor chip testing equipment, also contributed to performance during the quarter as it beat earnings estimates and affirmed guidance. AI-related opportunities are contributing to current growth and an enhanced outlook while the company’s exposure to mobility produces headwinds due to lower demand. TER produces returns on invested capital of 26% and sells below our estimate of intrinsic value.

QSV Mid Cap Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance during the quarter and is discussed above.

Lincoln Electric Holdings (LECO) detracted from performance during the quarter as the company saw softness in its quarterly revenues and lowered its full year earnings guidance. We see these as short-term issues for LECO, a trusted name in welding, cutting, and brazing products, with a leading global market share. While still in the commercialization phase, LECO is developing an EV charger business that represents an additional growth opportunity for the business. The company has raised its dividend for twenty-two years and produces returns on invested capital of 21%.

QSV Mid Cap Portfolio Activity

There were no total sales or purchases of positions during the quarter. QSV did add to its position in the clinical research organization Fortrea Holdings (FTRE) on weakness in its share price and made other trims and additions based upon valuation and our convictions in the fundamentals of the businesses.

QSV Select returned -4.40% and -4.62%, gross and net of fees, lagging the returns of the Russell 2500 Value and Russell 2500 Indexes of -4.31% and -4.27%, respectively. Select is a high conviction strategy that holds QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection was positive in Industrials. Selection and an overweight in Information Technology and Consumer Discretionary holdings also aided performance. Selection detracted from returns in Financials and Healthcare holdings.

QSV Select Top Contributors

Napco Security Technologies Inc. (NSSC) was the leading contributor to performance during the quarter and is discussed above.

Tyler Technologies Inc. (TYL) rose as its transition to Software as a Service, subscription revenues and earnings increased. TYL is the largest provider of enterprise software products focused solely on the public sector, with a focus on local governments where high switching costs stand as Tyler’s competitive advantage. The company has a 98% customer retention rate and incremental margins in its subscription business of over 70%. We continue to believe that TYL will benefit from increased government spending on infrastructure.

QSV Select Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance of QSV Select during the quarter and is discussed above.

Vestis Corporation (VSTS) detracted from performance during the quarter. Formerly a division of Aramark, VSTS provides uniform services and workplace supplies to North American Customers ranging from small businesses to Fortune 500 companies. Business performance has been impacted by client retention dropping because of off-cycle price increases and sub-par results from the company’s sales team. We believe the company’s focus on improved service and sales productivity will get this performance back on track.

QSV Select Portfolio Activity

Limited trading was done in QSV Select during the quarter, with trims and additions made to address valuations and quality upgrades.

Our Focus on the Long Term

We believe that mid-year reflection is appropriate for investors including a close look at asset allocation. With the concentration of returns to-date in large cap equities, and specifically in a handful of companies, many portfolios are tilted in favor of those holdings. Unintended bets may exist where investors in both passive and active funds have stakes in the Magnificent 7 companies that have increased in size. Markets could be “different this time” but if the outperformance of the S&P 500 over the smaller companies in the Russell 2000 persists throughout 2024 it will cap a four consecutive year period of such outperformance, something that has not occurred since 1995-1998. Small and mid-cap value equities excelled in the years that followed that, while investors in large cap stocks endured the “lost decade” of returns. Compelling valuations currently exist in small and mid-cap businesses. Coupled with the possibility of lower inflation, lower interest rates, and potential tailwinds from deglobalization, we see a convincing case for allocating to quality small and mid-cap companies.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Q1 2024 Commentary

Stocks marched higher in Q1 2024 with participation broadening from the mega cap winners of 2023 tomid-cap and smaller capitalization companies. U.S. economic growth, a steady consumer, and high expectations for interest rate cuts by the Federal Reserve promoted continued risk taking by investors. Gains in equity markets were largely multiple driven as earnings gains were modest and the stocks of lower quality small cap companies outpaced the returns of higher quality companies during the quarter. Using the Russell Stability indexes as proxies for high and low quality, the Russell 2000 Defensive index, containing businesses with higher Returns on Assets, lower leverage, and lower volatility underperformed low-quality businesses, as measured by the Russell 2000 Dynamic indexes, by 375 basis points for the quarter. More information including since-inception performance for each QSV strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned .78% and .72%, gross and net of fees, respectively, lagging the Russell 2000 Value Index return of 2.90% and the Russell 2000 Index return of 5.18%. Security selection in Communication Services, Financials, and Information Technology companies aided performance relative to the index. Security selection detracted from performance in Industrials as did an underweight and company selection in Energy holdings.\ Energy delivered the strongest absolute returns in the Index during the quarter due to elevated geopolitical risks and higher demand. QSV remains significantly underweight relative to the sector due to challenges in finding quality businesses at reasonable valuations.

QSV Small Cap Top Contributors

PubMatic Inc. (PUBM), a leading platform provider of digital advertising technology, was the leading contributor to performance in Q1 2024 as it continued to expand its customer base and the volume of ad impressions processed. A rebound in digital ad pricing also lifted revenue growth to levels beyond management’s prior forecast. Competitive advantages include switching costs – the time, effort, and money required to transfer platforms once an advertiser is set up on PUBM’s platform – and cost advantages through its investment in infrastructure and off-shore research and development. PUBM produces returns on invested capital of 12% on average.

Contract research organization Medpace Holdings Inc. (MEDP) contributed to performance as strong quarterly earnings exceeded expectations. MEDP is a leading provider of full-service drug development and clinical trial services to small and midsized biotechnology, pharmaceutical, and medical device firms. The company benefits from high switching costs as its tools and testing are highly scripted in regulation and practice. MEDP produces returns on invested capital of 25% on average.

QSV Small Cap Top Detractors

Forward Air (FWRD) fell 50% during the quarter due to pessimism over its acquisition of Omni Logistics. While FWRD stands as a leader in the less-than-truckload shipping business, concerns over its debt levels and integration risks persist. QSV is closely monitoring this integration and FWRD’s business performance. Despite its near-term headwinds, FWRD benefits from its substantial network of 92 terminals located at or near airports throughout North America. This network provides economies of scale and creates high barriers to entry, making replication of its capabilities a challenge.

Malibu Boats(MBUU) shares fell due to reduced forward guidance and concerns that higher interest rates will dampen sales of the company’s brands. Combined, its Malibu and Axis brands are the largest player in the ski/wakeboard market, one of the fastest-growing segments of the powerboat market. Malibu has been acquiring strong brands in a very fragmented industry and selling through its extensive dealer network of over 350 independent dealers, including 250 in North America. MBUU shares are currently at a significant discount to our estimate of intrinsic value, and QSV added to its position during the quarter.

QSV Small Cap Portfolio Activity

Shares of AMN Healthcare (AMN) and MGP Ingredients (MGPI) were sold for valuation reasons. Proceeds were invested in health management company Astrana Health (ASTH) and Vestis Corporation (VSTS), a provider of uniforms and other workplace supplies.

QSV Mid Cap returned 4.66% and 4.42%, gross and net of fees for the quarter, trailing the 8.23% return of the Russell Mid Cap Value Index and the Russell Mid Cap Index return of 8.60%. Security selection in Healthcare and Communication Services companies helped relative performance, as did our underweight to Communication Services names. Selection in the Financials, Industrials and Energy sectors detracted.

QSV Mid Cap Top Contributors

Contract research organization ICON PLC (ICLR) was the leading contributor to performance as it bounced back following concerns over its acquisition of competitor PRA Health. The cultures of ICLR and PRA Health are similar, and the combined organization will bring synergies and the benefit of reduced client concentrations. ICLR produces returns on invested capital of 10% on average, and its shares sell at a discount to our measure of intrinsic value. Lincoln Electric Holdings (LECO) also contributed to performance during the quarter with revenue and margin results that exceeded expectations. Founded in 1895, LECO is a trusted name in welding, cutting, and brazing products, with a leading global market share. While still in the commercialization phase, LECO is developing an EV charger business that represents a growth opportunity the business. The company has raised its dividend for twenty-two years and produces returns on invested capital of 20% on average.

QSV Mid Cap Top Detractors

MarketAxess Holdings (MKTX) was the leading detractor to performance during the quarter despite earnings results that exceeded analysts’ expectations and strong forward guidance. MKTX is the leading platform for trading fixed income securities, where it continues to grow market share due to the growing adoption of electronic execution. Greater adoption by retail and institutional investors and by the company’s network of dealers improves liquidity and the effectiveness of the platform for its clients. MKTX produces returns on invested capital of 27% on average and its shares are at a discount to QSV’s measure of intrinsic value.

Akamai Technologies (AKAM) detracted from performance during the quarter. AKAM operates through its Security, Compute, and Content Delivery Network (CDN) segments. AKAM is known for its CDNs that the company estimates deliver between 15% and 30% of global web traffic supported by over 350,000 servers arrayed in over 4,100 networks across the globe. Its growing network and application security business is a major focus for AKAM. With revenue growth in the mid-teens, this segment is expected to produce one-half of AKAM’s revenues in 2024.

QSV Mid Cap Portfolio Activity

There were no total sales or purchases of positions during the quarter. QSV did add to its position in the payroll and human capital management platform Paycom (PAYC) on weakness in its share price.

QSV Select returned 3.61% and 3.39%, gross and net of fees, lagging returns of the Russell 2500 Value and Russell 2500 Indexes of 6.07% and 6.92%, respectively. Select is a high conviction strategy that holds QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection was positive in Healthcare and Real Estate holdings. Selection detracted from returns in Industrials holdings while company selection and an underweight to Energy companies hurt performance.

QSV Select Top Contributors

Primerica Inc. (PRI) was the leading contributor to performance during the quarter. PRI provides financial services to middle-income households in the United States and Canada, offering life insurance, mutual funds, annuities, and other financial products. While earnings from life insurance were down for the quarter, asset-based revenues from annuities and mutual funds rose with the markets and PRI successfully grew its sales force. PRI’s shares continue to sell at a discount to our measure of intrinsic value.

Booz Allen Hamilton (BAH) rose on continued strong business performance and its reputation, as one analyst coined, as “AI at a Reasonable Price.” BAH has scale advantages as a provider of cybersecurity, data analytics, augmented reality, and artificial intelligence projects for the Department of Defense that, like all U.S. government contracts, are subject to elevated levels of scrutiny that serve as barriers to entry for competitors. The company has earned a position as the leader in artificial intelligence solutions and support for modernizing the U.S. military.

QSV Select Top Detractors

MarketAxess Holdings(MKTX) was the leading detractor to performance of QSV Select during the quarter and is discussed above.

Storage REIT National Storage Affiliates (NSA) detracted from performance during the quarter. Funds from operations in the trailing quarter were below analysts’ estimates and NSA’s guidance for 2024 revenues and net operating income were down on lower occupancy. In the long term, we remain positive on NSA as a REIT that has seen strong occupancy rates, the ability to pass along single to low double-digit rate increases, and the financial flexibility to pay down debt with an eye toward future acquisitions.

QSV Select Portfolio Activity

QSV continued to prune and add to Select to upgrade quality and address valuations. Freight broker Landstar System (LSTR), pool supply provider Pool Corporation (POOL), and Toro (TORO), an operator of oil tankers, were sold for holdings in which we have more conviction. New positions were initiated in Doximity (DOX), a digital platform for U.S. medical professionals, dating platform Match (MTCH), elevator and escalator provider OTIS Worldwide (OTIS), and Progress Software (PRGS), a provider of cloud-based security solutions.

Our Focus on the Long Term

We believe a good deal of 2024’s potential returns were pulled forward in Q4 2023. We also feel that market prices reflect near perfection in the economic and geopolitical outcomes of the coming quarters. Unfortunately, the world is imperfect and uncertain. At QSV, we do not invest in markets, but focus on building portfolios of quality businesses with durable competitive advantages purchased at reasonable valuations. We anticipate that 2024 will bring both surprises and the consequential market volatility. To prepare for this we recommend that long term investors focus on businesses with solid balance sheets, strong free cash flows, and high returns on invested capital. We continue to find these traits in the small and mid-capitalization businesses in each of the QSV portfolios and invite you to join us as we invest alongside our clients.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Q4 2023 Commentary

Q4 2023 Commentary

Q4 2023 reminded investors that the only thing constant is change. While the prior quarter saw markets fall due to the Federal Reserve’s commitment to keep rates higher for longer in its fight against inflation, the fourth quarter brought an “everything rally” with stocks, bonds, and crypto all rising in anticipation of interest rate cuts and a belief that a soft landing for the economy is likely. Small and mid‐cap stocks participated in the rally, notching most of their calendar year gains in the final three months of 2023. Each of the QSV strategies, focused on quality businesses that possess competitive moats, delivered strong outperformance for the calendar year relative to its respective value index. More information including since‐inception performance for each strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned 15.03% and 14.93%, gross and net of fees, respectively, slightly lagging the Russell 2000 Value Index return of 15.26% while leading the Russell 2000 Index return of 14.03%. The most significant positive impact was made in Energy companies, where an underweight to the index aided performance, and Communication Services companies, where QSV’s overweight detracted but security selection added value. An underweight and company selection in Consumer Discretionary companies detracted from relative returns. QSV’s overweight to Healthcare helped returns, but security selection detracted.

QSV Small Cap Top Contributors

After a significant drop in Q3 on news of its restatement of three quarters’ financial results, Napco Security Technologies (NSSC) was the leading contributor to performance during the quarter as its shares rose 54%. NSSC is a global provider and manufacturer of high‐tech security, and internet connected home, video, fire alarm, access control, and door locking systems. QSV was concerned about management’s controls that led to the need for the restatement and closely monitors the business. NSSC delivers returns on invested capital of 14% and sells at a discount to our measure of intrinsic value.

PubMatic (PUBM) was a leading contributor to performance as revenues, earnings and forward guidance all exceeded expectations. PUBM is a leading platform provider of the digital advertising technology, helping publishers that supply digital ad inventory to better manage their inventory, selling a high percentage of their inventory and maximizing revenue per ad sold. Competitive advantages include switching costs ‐ the time, effort, and money required to transfer platforms once an advertiser is set up on PUBM’s platform – and cost advantages through its investment in infrastructure and off‐shore research and development. PUBM produces returns on invested capital of 18%.

QSV Small Cap Top Detractors

Core Laboratories (CLB) fell 26% during the quarter, detracting from performance. The company has competitive advantages in reservoir analysis and production enhancement services, serving hydrocarbon exploration and production companies as they seek to improve production levels and economics. The company also anticipates significant future growth from the application of its technologies to carbon capture and sequestration projects. A risk inherent to the business is the cyclicality of oil prices, as was seen in Q4 2023.

Ituran Location and Control Ltd. (ITRN) shares fell in response to the war in Israel where the company has operations and a sizable portion of its client base. ITRN provides stolen vehicle recovery, fleet management, and other value‐added services. Its subscription‐based model adds 80,000 to 100,000 net new customers per year, derived from after‐market sales, OEMs, and insurance companies, and currently reports over 1.8 million subscribers across Israel and Latin America. ITRN management affirmed that the company has not seen any impact to its ongoing operations in Israel. Company headquarters are in the center of the country, just outside of Tel Aviv, and not near any borders. ITRN produces returns on capital of 19% and its shares are currently at a significant discount to intrinsic value.

QSV Small Cap Portfolio Activity

Trims and additions were made in five holdings during the quarter, but there were no new positions added. Shares of foodservice packaging company Karat Packaging (KRT) were sold for valuation reasons. QSV had sold portions of the KRT position two other times in 2023, taking gains in this long‐term holding.

QSV Mid Cap returned 12.32% and 12.05%, gross and net of fees for the quarter, leading the Russell Mid Cap Value Index return of 12.11% before fees while narrowly lagging the Index after fees. Mid Cap lagged the Russell Mid Cap Index return of 12.82%. Security selection in Information Technology and Financial companies helped relative performance, while selection in the Energy and Industrials sectors detracted. Underweights in Energy and Materials businesses helped relative performance, while over weights to Healthcare and Technology companies detracted from performance.

QSV Mid Cap Top Contributors

Monolithic Power Systems (MPWR) was the leading contributor to performance in the quarter as the company delivered strong earnings growth. MPWR is a global provider of high‐performance, semiconductor‐based power solutions. As a “fabless” company – one that does not manufacture the chips used in its products – MPWR has benefitted from devoting more resources to chip design rather than capital expenditures, resulting in greater free cash flows, higher margins, and Returns on Invested Capital of 24%.

Shares of Bank OZK (OZK) gained more than 35% during the quarter, supported by strong business performance including loan growth in its Real Estate Specialties Group that was greater than expected. OZK management noted that they will focus less on share buybacks in 2024 versus 2023 due to their expectations for further loan growth. OZK has a long history of exemplary credit, best‐in‐class profitability, and strong management. The bank produces Returns on Tangible Equity of 18% and its shares are trading at 1.1 times tangible book value.

QSV Mid Cap Top Detractors

Core Laboratories (CLB) was the leading detractor to QSV Mid Cap performance and is discussed above. Oil and natural gas producer APA Corporation (APA) detracted from performance during the quarter. While both revenues and earnings beat analysts’ expectations for the quarter, APA shares declined along with commodity prices. APA produces strong free cash flows and is committed to returning 60% to shareholders in the form of buybacks and share repurchases. Following the end of the quarter, APA announced its acquisition of Callon Petroleum (CPE) in an all stock deal, furthering the trend of M&A to build scale in the exploration and production industry. The combined company should see meaningful synergies through reduced overhead, interest expenses and operating synergies.

QSV Mid Cap Portfolio Activity

There were no total sales or purchases of positions during the quarter. QSV did add to its position in the payroll and human capital management platform Paycom (PAYC) on weakness in its share price.

QSV Select returned 13.98% and 13.74%, gross and net of fees, leading the 13.76% returns of the Russell 2500 Value before fees, while slightly lagging the Index after fees. QSV Select outperformed the 13.35% return of the Russell 2500 Index. Select is a high conviction strategy that takes QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection helped performance in Financial, Information Technology and Real Estate holdings, while detracting from performance in Industrials, Energy and Consumer Discretionary businesses. An underweight in Energy holdings aided performance.

QSV Select Top Contributors

Napco Security Technologies (NSSC) was the leading contributor to performance during the quarter and is discussed above.

Glacier Bancorp (GBCI) rose as quarterly results were better than anticipated. GBCI benefits from an operating footprint in seven economically vibrant U.S. states which supports robust organic growth. Additionally, the company has used cash flows to take a partnership approach to acquisitions which have led to the bank producing Returns on Tangible Common Equity of 14%.

QSV Select Top Detractors

Core Laboratories (CLB) was the leading detractor to performance of QSV Select during the quarter and is discussed above.

Human capital management provider Paycom (PAYC) detracted from performance during the quarter. PAYC’s revenues were down due to its conversion of clients to a new, innovative solution that lessens errors and reduces the need for additional payroll runs as a result. PAYC targets customers with 50 – 10,000 employees and is expanding its business with larger enterprise deals and a push into both Mexico and Canada. The company has approximately 5% penetration of its total addressable market which we believe it can expand through its best‐in‐class salesforce. PAYC has returns on invested capital of 24%.

QSV Select Portfolio Activity

Turnover during the quarter was minimal, but QSV made one addition to upgrade its portfolio. Using the proceeds from Masimo (MASI), which was exited at the end of Q3, Amdocs (DOX) was purchased. DOX is a forty‐year‐old provider of software and services solutions for communications, entertainment, and media industries.

Our Focus on the Long Term

2023 stands as a stark reminder that predictions of market returns are folly. Few would have anticipated that markets would rise so significantly or that world events would take the turns – often tragic – that they did. While we cannot (and do not) predict, we can prepare. The strong results of 2023 have pulled forward market returns in expectation that interest rates will be cut, that inflation will continue to fall, and that corporate earnings will grow. One or more of these may not come about. The leveraged consumers that have bullishly supported the economy, and the labor market that has supported them, may cool. Geopolitical events may present challenges.

Preparing for uncertainty leads QSV to its focus on long term investment in quality businesses, those with limited debt, high interest rate coverage and strong free cash flows. We continue to find compelling opportunities in small and mid‐cap stocks of these quality firms, at reasonable valuations, and believe they will serve our clients well as we invest alongside them.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Q3 2023 Commentary

QSV Equity Investors

Q3 2023 Commentary

Q3 2023 was difficult for U.S. equities as the reality that “higher for longer” truly will mean higher interest rates for longer gelled in the minds of investors. The Federal Reserve is intent on fighting inflation and seems committed to keeping rates high and conditions tight for the foreseeable future, causing concerns over the impact on the economy. Economic growth and interest rates impact smaller companies more than large, and small caps experienced a double digit drop from their July peak through the quarter-end. Three months is a brief period for investors focused on the long term, yet Q3 2023 was a quarter, given the market environment, where we expected our stock selection in the QSV strategies to perform better.

Particularly within the QSV Small Cap and Select strategies, a handful of companies disappointed. Some of these, we believe, still deserve a place in the portfolios and we have added to certain names at lower prices where the disappointment is believed to be temporary. Others we have exited in favor of higher conviction positions.

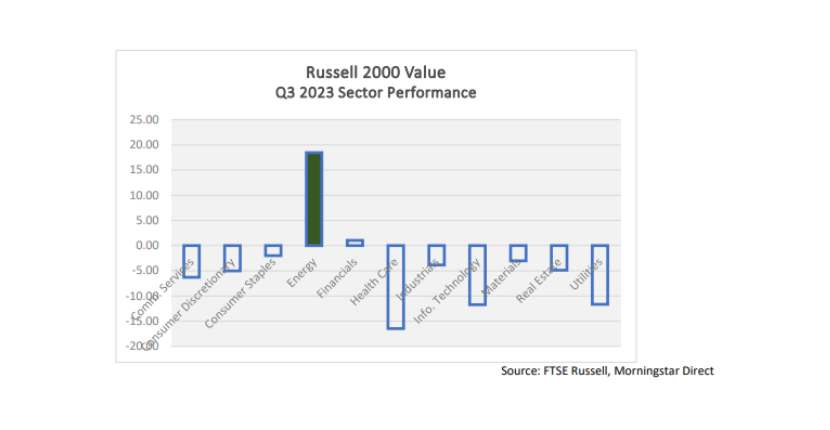

Beyond security selection, the headwinds to our portfolios from being underweight in energy were considerable this quarter. The Energy sector was up over 18% within the Russell 2000 Value index, while every other sector – save Financials at +1.04% – were in negative territory. QSV has historically been underweight in energy companies. In a period of $90 per barrel oil, many energy companies can boast high returns on invested capital; at more “normal” prices it is challenging to find energy businesses with competitive advantages, disciplined management, and the high business returns that we require.

QSV’s Small Cap and Select strategies underperformed their respective Russell value indexes during the quarter while QSV Mid Cap was in line with its index. More information including since-inception performance for each of the strategies may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned -5.24% and -5.31%, gross and net of fees, lagging the Russell 2000 Value Index return of -2.96% and the Russell 2000 Index return of -5.13%. The most significant positive impact was made in Consumer Discretionary companies, where QSV added value in security selection and was underweight compared to the index, and in Healthcare, where QSV was overweight and added value through security selection. An underweight and company selection in Energy companies accounted for nearly all the Small Cap portfolio’s underperformance relative to the index. Company selection in Real Estate also detracted from relative returns.

QSV Small Cap Top Contributors

Capri Holdings, Ltd. (CPRI) was the leading contributor to performance during the quarter as shares rose 46%. The purveyor of Michael Kors, Jimmy Choo and Versace agreed to be acquired by Tapestry (TPR) for $57 per share. We expect the deal with TPR to close in 2024 and exited our position placing the proceeds in companies we believe provide better opportunities.

For the second consecutive quarter, foodservice packaging company Karat Packaging (KRT) was a leading contributor to performance. Gross margins improved as KRT continued to benefit from lower input and shipping costs. Core products continue to show sales growth and the company’s Eco-friendly product sales are trending above 30%. The company initiated a quarterly dividend during the quarter, underscoring the strength of its free cash flow. KRT generates returns on invested capital of 15%.

QSV Small Cap Top Detractors

After being one of the portfolio’s greatest contributors for the year, shares of Napco Security Technologies, Inc. (NSSC) dropped on the news that it would restate the prior three quarters’ results due to understating cost of goods sold. NSSC is a global provider and manufacturer of high-tech security, and internet-connected home, video, fire alarm, access control, and door locking systems, serving commercial, industrial, residential, and government markets. Management has said the issue is resolved and will not impact results going forward. We have concerns about management’s controls that led to the need for the restatement and will continue to closely monitor the business. Prior to this restatement, we had sold

a meaningful amount of the position on strength.

Forward Air (FWRD) shares were hit on news that they are merging with private company Omni Logistics, a provider of global freight forwarding and third-party logistics services. The merger will roughly double the scale of FWRD and will add new growth opportunities with an asset light business, yet it does present integration risks. QSV acknowledges these risks but sees opportunities for growth and cost synergies within the business. We added to our position in FWRD on weakness in its shares.

QSV Small Cap Portfolio Activity

The acquisitions of Capri Holdings (CPRI) by Tapestry and PDC Energy (PDCE) by Chevron prompted the exit of those positions during the quarter. Johnson Outdoors (JOUT), UMH Properties (UMH), and UniFirst Corporation (UNF) were sold due to business performance that did not meet our expectations and the opportunity to upgrade to better ideas. New positions were initiated in professional medical platform Doximity (DOCS), business process management company ExlService (EXLS), LabCorp spin-out Fortrea Holdings (FTRE), Hanover Insurance (THG), real estate finance company Walker & Dunlop (WD), and digital media company Ziff Davis (ZD).

QSV Mid Cap returned -4.32%, gross of fees for the quarter, leading the Russell Mid Cap Value Index return of -4.46% and the Russell Mid Cap Index return of -4.68%. The net return of -4.55% lagged the Russell Mid Cap Value Index while exceeding the Russell Mid Cap Index. Security selection in Consumer Discretionary and Industrials companies helped relative performance, while selection in Financials and Real Estate businesses detracted.

QSV Mid Cap Top Contributors

Outsourced payroll and human capital management provider Trinet Group, Inc. (TNET) was the leading contributor to performance in the quarter. Increasing use of technology, digitization of the HR function, employment growth in new industries and increasing geographic decentralization of the small and medium-sized business workforce all create favorable trends for TNET. TNET has competitive advantages relative to its peers that include its scale and the efficiencies offered through the consolidation of its operating units on a single technology platform. TNET generates returns on invested capital of 28% and shares are at a discount to our estimate of intrinsic value.

Shares of APA Corporation (APA) gained more than 20% during the quarter on rising oil prices, contributing to the results of QSV Mid Cap. APA produces oil and gas with operations in the U.S., Egypt and the United Kingdom, and exploration activities offshore in Suriname. APA generates strong free cash flows and is committed to returning 60% to its shareholders, primarily through share repurchases, dividends and paying down its debt.

QSV Mid Cap Top Detractors

Masimo Corporation (MASI) fell on poor financial results and lowered future guidance. Results were impacted by issues that included lower hospital volumes, elevated channel inventory levels, and hospital labor inflation that is impacting capital equipment demand. MASI is a medical technology company which develops, manufactures, and markets non-invasive vital sign monitoring devices and offers consumer audio products. The integration of its acquisition of Sound Audio has continued to present challenges to the business and we exited the position in favor of higher conviction businesses.

Etsy Inc. (ETSY) detracted from performance during the quarter. Etsy markets differentiated products through its “House of Brands” which includes Esty.com, Reverb, and Depop. Competitive advantages include the diversity of its offerings, a strong base of active buyers and sellers, and productivity tools it offers sellers. Despite these advantages, with rising fuel prices, the resumption of student loan payments, and a shift by consumers to “experiences” over goods, we believe there are better opportunities for our investors, thus we exited the position during the quarter.

QSV Mid Cap Portfolio Activity

Turnover during the quarter was higher than usual as QSV took opportunities to upgrade its portfolio. As noted above, Etsy (ETSY) and Masimo (MASI) were exited for business performance reasons. A.O. Smith (AOS), Cintas (CTAS), and Ross Stores (ROST) were sold for valuation reasons and Mid-America Apartment Communities (MAA) was sold to allocate to better ideas. New positions were initiated in digital services provider Amdocs (DOX), nitrogen producer CF Industries (CF), LabCorp spin-out Fortrea Holdings (FTRE), GPS-enabled hardware and software provider Garmin (GRMN), Match Group (MTCH), elevator and escalator manufacturer OTIS Worldwide (OTIS), and Waters (WAT), a provider of liquid chromatography and mass spectrometry products.

QSV Select returned -6.25% and -6.45%, gross and net of fees, lagging the returns of -3.66% and -4.78%, respectively for the Russell 2500 Value and the Russell 2500 Indexes. Select is a high conviction strategy that takes QSV’s best ideas from our Small Cap and Mid Cap strategies. An underweight and company selection in Consumer Discretionary companies helped performance as did QSV’s absence in the poorly performing Utilities sector. Company selection detracted from performance in the Financials sector as did our underweight and underperformance in Energy businesses.

QSV Select Top Contributors

Brady Corporation (BRC) was the leading contributor to performance during the quarter as the company beat consensus earnings estimates and raised its guidance for the full year. The company manufactures and sells identification and workplace safety products through its Identification Solutions and Workplace Safety segments. BRC has niche advantages in safety, identification, and compliance markets and has a diversified customer base, products, and geographic footprint. The company’s strong free cash flows have supported dividend increases for thirty-seven consecutive years, share buybacks and strategic acquisitions.

EPAM Systems, Inc. (EPAM) rose as quarterly results were better than anticipated. The company has diversified its workforce away from its previous exposure to Ukraine and the belief that demand for the company’s services may be bottoming raised investor sentiment. The global technology services company has a network of multidisciplinary teams delivering software product development and digital platform engineering services. Most of the firm’s revenues are generated from U.S. customers and its top twenty clients (representing 41% of revenue) have been with EPAM for an average of ten years. Returns on invested capital stand at 17%.

QSV Select Top Detractors

Masimo Corporation (MASI) and Napco Security Technologies, Inc. (NSSC) were the leading detractors from performance in Q3 and are discussed above.

QSV Select Portfolio Activity

QSV took opportunities to upgrade the Select portfolio during the quarter. Shares of PDC Energy (PDCE) were sold as Chevron (CVX) acquired the business. Generac Holdings (GNRC) was sold for valuation reasons. Positions were initiated in CF Industries (CF) and Fortrea Holdings (FTRE).

Our Focus on the Long Term

Investors began the last quarter on an optimistic note, while bullishness faded in September. Strength of the consumer continues to be touted as a positive for the economy (Americans Are Still Spending Like There’s No Tomorrow), as are strong employment and rising labor participation rates. Yet credit card debt is high and student loan payments are again due. Persistent inflation and higher interest rates will also weigh on the consumer as well as on corporate earnings. The Financial Times notes that 30% of the debt of Russell 2000 companies is variable rate debt (as compared to 6% for S&P 500 companies), presenting risks to lower quality, more leveraged businesses.

At this stage in the market cycle, we believe that QSV’s style of investing and our investors should do well. Late cycle investing favorsthe lower volatility stocks of quality businesses, those that have limited debt, high interest rate coverage and strong free cash flows. Selectivity is important and opportunities abound in small to mid-cap stocks that have been overlooked in the narrow market that dominated the first half of the year. Investors will also do well to check their asset allocation; the mega-cap led markets of 2023 have left many portfolios in an unbalanced state and shifts in allocations may be due.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

QSV Q2 2023 Commentary

QSV Equity Investors

Q2 2023 Commentary

Stocks climbed a wall of worries in the first half of 2023 that included a banking crisis, higher interest rates and inflation, the debt ceiling debate, and geopolitical concerns. Looking specifically at the “Magnificent Seven” large cap technology stocks, returns of those shares did not climb, but vaulted the wall, leaving other segments of the market in the distance. Bullishness in June lifted shares of lower quality businesses creating headwinds to the quality biased QSV strategies in Q2 2023. Using the Russell Stability indexes as proxies for high and low quality, the Russell Defensive indexes containing businesses with higher Returns on Assets, lower leverage, and lower volatility underperformed low quality businesses, as measured by the Russell Dynamic indexes, across the market cap spectrum for the quarter. QSV’s Small Cap and Mid Cap strategies outperformed their respective Russell value indexes during the quarter while QSV Select slightly underperformed. More information including since-inception performance for each of the strategies may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned 3.31% and 3.22%, gross and net of fees, leading the Russell 2000 Value Index return of 3.18% while trailing the Russell 2000 Index return of 5.21%. The most significant positive impact was made in Healthcare, where QSV added value in security selection and was overweight compared to the index, and in Financials, where QSV was underweight and added value through security selection relative to the index. Security selection in Information Technology and Industrials detracted from performance.

QSV Small Cap Top Contributors

Generac Holdings Inc. (GNRC) was the leading contributor to performance during the quarter. Demand for home standby generators is strong and headwinds from high inventory levels in the company’s supply chain are abating. GNRC benefits from a scale advantage in the home generator market with a market share four times greater than their next competitor. The company produces returns on invested capital of 15% and is actively deploying free cash flow from its legacy generator business into its newer clean energy business. QSV trimmed its position in GNRC as the price appreciated.

Karat Packaging (KRT) contributed to performance as shares rose nearly 40%. The foodservice packaging company benefitted from lower input and shipping costs for its products and from increased sales supported by greater distribution capacity in its Midwestern region. KRT produces returns on invested capital of 13% and uses its free cash flow for tuck in acquisitions and capacity expansion.

QSV Small Cap Top Detractors

Shutterstock (SSTK) was the leading detractor to performance for the quarter. Shares fell due to concerns that the stock imagery business of SSTK will be disrupted by Artificial Intelligence generative imagery. While this is a risk to monitor, SSTK is developing its own AI capabilities and is leading its peers with this initiative. SSTK purchased GIPHY from META during the quarter, increasing its total addressable market by adding the world’s largest collection of GIFs and stickers. SSTK produces returns on invested capital of 15%

Glacier Bancorp (GBCI) fell during the quarter as investors reacted to the bank’s lower net interest margins and higher deposit costs. While these results are disappointing, they were not unexpected given the current market environment. We see GBCI as a strong banking franchise with prudent expense management and a thirty-year history of making acquisitions to fuel growth in its business. GBCI produces returns on tangible equity of 16% and has net interest margins more than 3%.

QSV Small Cap Portfolio Activity

Following strong stock performance, Choice Hotels (CHH), Core Laboratories (CLB), Lemaitre Vascular (LMAT), Morningstar (MORN), and Watts Water Technologies (WTS) were sold for valuation reasons. Methode Electronics (MEI) was sold due to concerns over its ability to effectively integrate its acquisition of Northern Lights. World Wrestling Entertainment (WWE) was sold as it approached its acquisition by Endeavor. New positions were initiated in AudioCodes (AUDC), a provider of voice over IP and data networking solutions, Capri Holdings (CPRI), the holding company for retail brands Michael Kors, Jimmy Choo and Versace, consulting services firm ICF International (ICFI), Malibu Boats (MBUU), and Scotts Miracle Gro (SMG). QSV Mid Cap returned 4.09% and 3.84%, gross and net of fees, for the quarter, leading the Russell Mid Cap Value Index return of 3.86% and lagging the Russell Mid Cap Index return of 4.76%. Security selection and an overweight relative to the index in Industrials helped performance as did security selection and an underweight in Utilities. Company selection in Financials and an underweight and security selection in Consumer Discretionary names detracted.

QSV Mid Cap Top Contributors

Management consulting firm Booz Allen Hamilton (BAH) was the leading contributor to performance in the quarter. BAH has scale advantages as a provider of cybersecurity, data analytics, augmented reality, and artificial intelligence projects for the Department of Defense, that, like all U.S. government contracts, are subject to elevated levels of scrutiny that serve as barriers to entry for competitors. The company’s standing as the leader in artificial intelligence solutions to the U.S. government helped propel its share price during the quarter. Shares of vehicle salvage auctioneer Copart (CPRT) gained more than 20% during the quarter. The rate at which insurers choose to total vehicles following accidents has increased due to elevated repair costs, providing CPRT better access to salvaged vehicles for resale. Sales volumes and price per unit sold were up and margins increased during the quarter. CPRT produces returns on invested capital of 26% and net operating margins of 31%. QSV trimmed its position in CPRT during the quarter for valuation reasons.

QSV Mid Cap Top Detractors

MarketAxess Holdings (MKTX) fell on concerns over slightly lower trading volumes that resulted from uncertainty in the banking sector and seasonal patterns. MKTX is the leading platform for trading fixed income securities, where it continues to take market share due to the growing adoption of electronic execution. It is expected that higher yields will drive greater allocations of assets to fixed income and increased participation by retail & institutional investors. Greater adoption by these buyers and by the company’s network of dealers improves liquidity and the effectiveness of the platform for its clients. MKTX produces returns on invested capital of 28% and its shares are at a discount to QSV’s measure of

intrinsic value.

Etsy Inc. (ETSY) declined during the quarter over concerns that consumers’ spending was shifting from goods to services and that the company would be challenged to profitably add customers. Etsy markets differentiated products through its “House of Brands,” which include Esty.com, Reverb, a musical instrument marketplace, Depop, a resale marketplace, and Elo7, a Brazilian marketplace for handmade goods. ETSY joined 7.5 million active sellers with 95.1 buyers as of December 2022. Customer acquisition costs are elevated from COVID era levels, but we see the diversity of its offerings, the strong base of active buyers and sellers, and the productivity tools it offers sellers as competitive advantages. ETSY shares sell at a meaningful discount to our measure of intrinsic value.

QSV Mid Cap Portfolio Activity

QSV took opportunities to upgrade its portfolio during the quarter. New positions were started a previous QSV holding, Jack Henry & Associates (JKHY), a provider of bank technology and payment processing services, and equity exchange Nasdaq Inc. (NDAQ). QSV Select returned 4.03% and 3.80%, gross and net of fees, lagging the returns of 4.37% for the Russell 2500 Value Index and the return of 5.22% for the Russell 2500 Index. Select is a high conviction strategy that takes QSV’s best ideas from our Small Cap and Mid Cap strategies. Company selection in Communication Services and Consumer Staples contributed to performance, while selection in Financials and Real Estate detracted.

QSV Select Top Contributors

Generac Holdings Inc. (GNRC) was the leading contributor to performance during the quarter

and is discussed above. Management consulting firm Booz Allen Hamilton (BAH) was a leading contributor to performance and

is also discussed above.

QSV Select Top Detractors

After being a top contributor to performance of the Select strategy in Q1, shares of electronic trading platform MarketAxess Holdings (MKTX) detracted from performance in Q2. MKTX is discussed above.

Glacier Bancorp (GBCI) fell during the quarter and is also discussed above.

QSV Select Portfolio Activity

QSV took opportunities to upgrade the Select portfolio during the quarter. Shares of Church & Dwight (CHD), Pubmatic (PUBM), and WD-40 (WDFC) were sold for valuation reasons and to purchase higher conviction companies. Positions were initiated in EPAM Systems, Inc. (EPAM), Jack Henry & Associates (JKHY), and Paycom Software (PAYC).

Our Focus on the Long Term

Optimism has returned to the markets and to consumer sentiment, and somewhat rightfully so. 401(k) and brokerage account balances have improved measurably from the end of 2022. This optimism has supported stronger consumer spending on services and is reflected in the performance of certain stocks, with cruise line operators Carnival, Norwegian and Royal Caribbean standing out as the top three S&P 500 performers in Q2. For those still seeking out areas for concern (and not believing that it is different this time) risks exist. Core inflation, the measure excluding food and energy, remains well above target and is declining at a glacial pace. The Federal Reserve and its peer central banks have not yet gotten the desired results from a string of rate hikes. Chairman Powell’s comments that we have “a long way to go” in getting back to 2% policy rates signal more rate increases to come. Elevated borrowing costs are likely to eat into corporate profits and we believe this puts the current valuations of lower quality, more leveraged small and mid-cap companies at risk. Opportunities exist for equity investors, and we counsel an emphasis on quality businesses with limited debt, high interest rate coverage and strong free cash flows. As always, this remains our focus for delivering long-term results for our clients as we invest alongside them.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do the QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.