Lessons Learned in 25 Years of Investing Together

QSV_Lessons Learned in 25 Years

QSV Equity Investors was founded in 2016 as an independent, employee-owned advisory firm by Jeff Kautz and Randy Hughes. Jeff and Randy began investing together twenty-five years ago at Perkins Investment Management, where their boss and mentor, Bob Perkins, first hired Randy in 1995 and then Jeff in 1997. The business and their careers grew. From assisting Bob in the management of a $30 million small cap value fund the late 1990s to responsibilities on multiple value products and over $20 billion in assets by 2016, Jeff became CEO and Chief Investment Officer of the firm and Randy held the roles of Director of Research and Analytics and Equity Analyst. Jeff also served as co-manager of the Janus Henderson Mid Cap Value Fund and the Janus Henderson Value Plus Income Fund.

Twenty-five years into their partnership, Randy and Jeff remain value investors and lessons have been learned over that period. The tools used, and the approach taken to investing clients’ assets have evolved, with the philosophy that investing is a craft where you can learn and get better over time. Seven key lessons, our reflections, and what we believe are the benefits to our clients, follow.

CHEAP IS NOT ENOUGH; QUALITY BOUGHT AT A REASONABLE PRICE ADDS VALUE

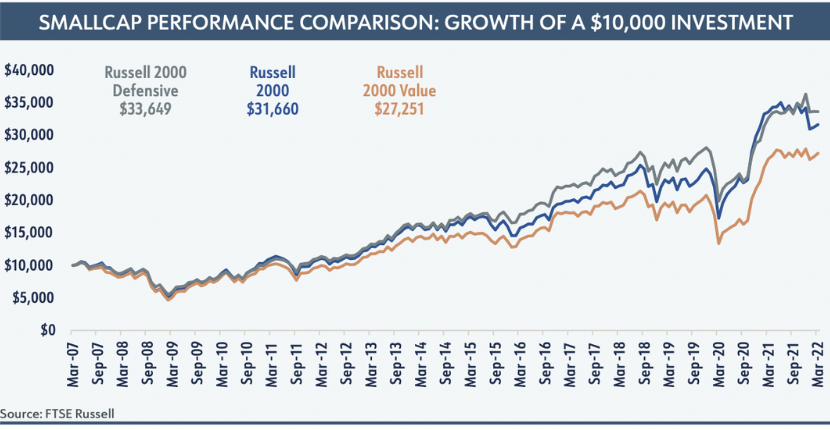

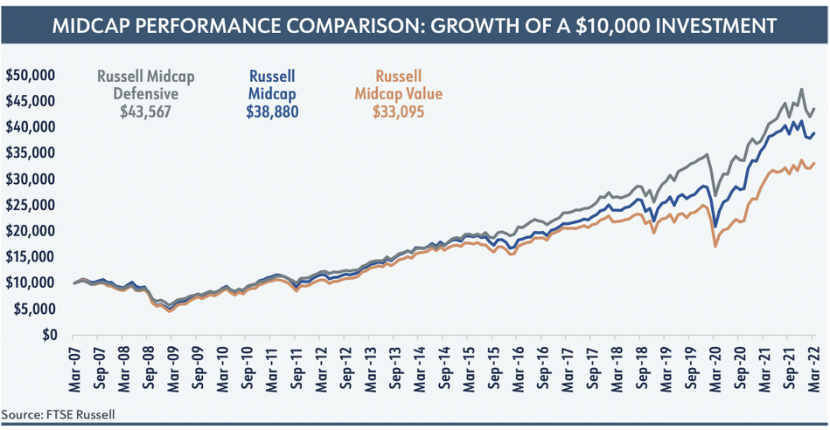

Early in their careers at Perkins, Jeff and Randy focused on cheap stocks, using the 52-week lows list as the starting point for their investment process. Subsequent process steps dug into the fundamentals of each company and an assessment of the durability of its business model. As they gained experience, Jeff and Randy gained conviction in the critical importance of quality and the durable competitive advantages that certain companies earned through successful execution. Their conviction was supported by the “smoother ride” that companies with the characteristics of quality, including strong balance sheets, persistent returns on invested capital, strong and growing free cash flows, and lower levels of debt, delivered. Performance of the Russell Defensive Small and Mid-Cap indexes relative to the Russell value indexes supports this over the last fifteen years as shown on the next page.

Much like the qualities sought by QSV, the Russell Defensive indexes emphasize stocks that exhibit a combination of high return-on-assets, low debt-to-equity, low earnings variability, and low long- and short-term total return volatility. QSV starts its investment process with a singular focus on quality, using both quantitative and qualitative tools to assess the durability of prospective holdings. This focus is grounded in the understanding that we are owners of each business, not traders in its stock.

ALL VALUATION TOOLS ARE NOT EQUAL

Over the course of our twenty-five years of working together, Jeff and Randy have used many methods of valuation. While some can be more useful than others, they have found that these conventional tools are insufficient to meet the needs of the modern investor.

Valuation multiples are the most widely used measures for valuing equities because they are simple to use. These multiples require only two inputs – an estimate of the firm’s value in the numerator and a measure of some valuation metric in the denominator. For example, the trailing 12-month price-to-earnings multiple simply divides a stock’s current share price by the last year’s earnings per share. The simplicity of this type of value calculation also speaks to its shortcomings – multiples tend only to provide high-level snapshots of valuation at a point in time. These shortcomings can misguide investors; a P/E may appear low because the company is at peak earnings. Or, without considering what may happen to the “E,” or earnings, in such a simple equation, investors often can step into value traps – stocks that are cheap for good reason – when relying on multiples.

Another common method of valuation is the Enterprise Value formula, which is used to represent a business’ book value, or the total cost of acquiring that business today. The cost of acquisition can be calculated by adding the total market value of the company’s equity to the total debt that it carries. The resulting sum is a shorthand (though widely accessible) figure that, like multiples, does little to inform us of a business’ investment-worthiness.

Discounted cash flow analysis provides a more accurate measure of the intrinsic value of a business by considering the present value of the cash flows the company is expected to generate in the future and discounting them to arrive at a current, present value. DCF calculates a company’s intrinsic value based on cash flow projections far into the future, which are discounted back to a present value using a combination of a risk-free rate and an equity risk premium. Predicting cash flows is tricky – they are likely to change in time – but a company is not as likely to try to distort cash flows the way it may do with earnings. And applying this cash flow analysis to more predictable, quality businesses is more prone to good outcomes than when assessing more volatile or cyclical businesses.

We lean on QSV proprietary, and more sophisticated, valuation model to identify winning companies. Our Economic Profits Model enables us to take a closer look at what a prospective firm has going on under the hood. Economic Profits and Cash Flow Models are similar and should arrive at the same intrinsic value for a company. However, we believe the Economic Profits Model, which considers both the cost of debt, as DCF does, as well as the cost of equity, provides additional insight. By studying the firm’s capital structure and allocation decisions, such as its debt levels, tax rates, share repurchases and dividend payouts, QSV can assess whether management’s capital allocation decisions are creating or destroying value, making this model a more comprehensive tool for valuing a firm’s stock.

RISK MEANS DIFFERENT THINGS TO DIFFERENT INVESTORS

Allocators today consider many measures of “risk” when weighing the results of QSV and its peer investors. Statistics including standard deviation of returns, downside deviation, drawdown and tracking error relative to an index are among the tools used and, while helpful, are all backward looking in their measurement, using data that is in the past. QSV considers the fundamentals of each prospective investment (using backward looking data) and then considers the prospects of that business looking forward, concentrating our ownership on what we believe will be the best wealth creating holdings for our clients. As owners of a portfolio of quality businesses and as fiduciaries to our clients, QSV views risk as the permanent loss of capital. Our insistence on quality businesses leads to another benefit, albeit a residual of our process; QSV portfolios consistently have lower standard deviations of returns than their indexes.

INDEXES ARE NECESSARY TOOLS, BUT POOR MASTERS

“What gets measured gets done” is a popular saying used to emphasize the importance of performance measurement in business and the business of investment management is no different. Investment indexes are the industry’s tools to benchmark the results of each portfolio over time and, like popular risk measurement statistics, QSV sees these as a necessary tool for our clients and their advisors. We do not manage portfolios with an eye toward adhering to the sector weights or holdings of the relevant index, however, but build portfolios one business at a time. Relative to value indexes and many of our value peers, this generally results in greater exposures to segments of the economy such as healthcare, technology, and consumer staples businesses, where we find quality businesses that possess durable competitive advantages or “moats.” QSV finds fewer of these businesses and has lower weights relative to the indexes in the energy, materials, and financial sectors. Understandably, this results in performance of the portfolios that may be quite different than the indexes in short term periods. QSV always counsels clients to expect this, but we believe we can deliver performance greater than both the value and core indexes over full market cycles, with less risk.

PATIENCE AND CAREER RISK DO NOT LIVE WELL TOGETHER

Delivering excess performance, or alpha, is challenging and even the most skilled investors will have periods, sometimes extended periods, of underperformance. Clients, their advisors, and, as a result, large, publicly-traded investment houses, routinely measure the results of their portfolios against relatively short one- and three-year periods. This is a reality of the business but creates risks to the employment status of many investment professionals. An independent, employee-owned firm must answer to these same client demands but can structure employment and compensation programs to reflect the longer periods of time that may be needed to demonstrate the merits of an investment strategy. At QSV, we believe the correct way to assess the success of a portfolio manager is over a full market cycle, including both peaks and troughs.

CLIENT FIT IS LIKE MARRIAGE

Just as it is difficult to deliver outperformance in active management, it can be hard for asset owners to hold actively managed portfolios, given the disconnects between managers and their respective indexes and periods of underperformance. Just as in a marriage, humility, patience, time, honesty, trust, and communication are all necessary for a successful relationship between a client and its investment managers. QSV is judicious in setting client expectations early in each relationship. We strive to communicate openly and often, and take ownership of our results, both good and bad. Our intention is to have long, trusting relationships with clients who can invest alongside us and benefit from our work.

CULTURE MATTERS

Culture is critical to the success of a business where the assets – human capital – walk out the door every evening. QSV’s team members have worked in small, independent firms and in large publicly traded businesses. We have learned that maintaining the cultural traits that support delivering results for our clients and retaining motivated employees is best done in an independent, employee-owned firm. Traits we hold as critical are:

- Ownership of our defined, repeatable approach to investing.

- Team members sharing a passion for research, investing and client service.

- An ego-free culture that combines diverse, independent thought with collaborative decision-making.

- An emphasis on investment excellence over asset gathering.

- Employee ownership and a willingness to share ownership with key contributors.

CONCLUSION

Lessons learned are often the result of mistakes made and in twenty-five years of investing together Randy and Jeff have made their share. Admitting to those errors, learning, and making the adjustments necessary to QSV’s investment process over time is what will enable us to add value for our clients going forward. The investment world has changed immensely in twenty-five years, with the availability of more information facilitated by rapidly changing technology, changes in investors’ preferences, and with more competition from active and passively managed investment vehicles. QSV’s emphasis on owning quality businesses that create wealth for clients persists, while our process for finding the best of those companies at compelling valuations continues to be refined. We are reminded of the advice of baseball manager Jimmy Dugan in A League of Their Own: “Of course it’s hard. It’s supposed to be hard. If it were easy, everybody would do it. Hard is what makes it great.” We will continue to do the hard work, learn from our mistakes, and refine our craft as we serve our clients.

“Of course it’s hard. It’s supposed to be hard. If it were easy, everybody would do it. Hard is what makes it great.”

ABOUT QSV EQUITY INVESTORS, LLC

QSV Equity Investors, LLC is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Perkins Investment Management and have invested together for over 20 years. For more details on the specific performance and characteristics of QSV’s strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@ballastequity.com.