Competitive Advantage Period Defending Your Castle

QSV_Competitive Advantage Period

“In business, I look for economic castles protected by unbreachable ‘moats’. The wider a business’ moat, the more likely it is to stand the test of time.” -Warren Buffett

Companies that generate returns on invested capital greater than its cost of capital are instrumental in achieving long-term wealth for investors, as discussed in our previous paper, “A Valuation Framework for Beating Inflation and Creating Long-Term Wealth.” Unfortunately, companies that create wealth eventual

ly attract competition from other companies, ultimately driving down product prices and profit margins.

Competition and lower prices are good for consumers and society as a whole, but can be detrimental for individual companies’ profitability. Many investors fail to appreciate this reality and are surprised when the stock of a previously successful company reverts downward.

This scenario is common with small-cap growth companies. Typically, a small company with an exciting new product (such as a smartphone app) grows very rapidly in the beginning, ultimately driving up its stock price and valuation. Other companies, having observed this successful product, copy the idea, quickly encroaching into the same space. This usually leads to an unfavorable earnings surprise for the original innovator and the stock gets crushed when the market figures out what has happened. Compounding the impact is that these stocks are typically long duration stocks, which means investors place more value on cash flows in the distant future and less value on current cash flows and earnings. Such stocks are commonly referred to as “story” stocks, but sadly many stories never materialize because competition is alive and well in the world. Imagine that — capitalism works.

Because competition is real, it is important for investors to assess the competitiveness of every company in their portfolio. On the positive side, many companies have the ability to generate positive economic profits for many years before eventually reverting back to the cost of capital. Most likely, these companies have created competitive advantages that prevent other companies from eroding all of their excess returns.

Warren Buffet calls such competitive advantages “economic moats” and consistently emphasizes that he wants to own businesses that are like a castle surrounded by a moat that can fend off competition. Historically, moats were deep, broad ditches, typically filled with water and surrounding a castle, building or town. Moats provided a preliminary line of defense against enemies and invading armies. An economic moat is like a castle moat, but instead of fending off Romans or Huns, a company’s “moat” helps it fend off competing companies. Any advantage a company has that acts as a barrier preventing other companies from stealing market share and profits is referred to as its competitive advantage.

Competitive Advantage Period (CAP)

Companies with a positive economic spread, meaning the companies earn a return on invested capital in excess of capital costs, will eventually attract competition. This is where investors’ real work begins. Once we identify companies with high returns on capital, we need to determine whether those companies have competitive advantages and how durable those advantages are.

Determining how durable and how protracted a company’s Competitive Advantage Period (CAP) will be is key to successful valuation. We want a CAP that lasts far more than a year or two. Ideally, we want CAPs that last 10, 15 or even 20 years. Stocks with long CAPs that are bought at reasonable valuations can produce attractive returns and great wealth for investors well into the future. Companies with long CAPs should trade at higher multiples than their peers. However, many companies with short CAPs trade at high multiples due to the market’s infatuation with earnings growth and story stocks.

“In spite of CAP’s importance in the analytical process—it remains one of the most neglected components of valuation.” – (Mauboussin, et al., 1997).

Companies with long CAPs can be held for many years, thereby reducing trading costs, capital gains taxes, and market timing mistakes. High CAP stocks are justly labeled “sleep at night” stocks. For example, suppose a company like Coca-Cola misses an earnings estimate. Immediately, analysts publish negative reports, causing investors to panic and sell the stock. But investors who did their homework know that Coke has a very long competitive advantage period due to its tremendous brand identity and scale. These investors are likely to recognize the stock’s decline as a buying opportunity. In contrast, if a speculative technology company misses its earnings, investors would need to quickly determine whether new entrants had broken through and permanently reduced the company’s future prospects and profitability. A strong business does not survive from quarter to quarter, and one bad earnings announcement should not change the long-term outlook of a quality company with high future economic profits.

The concept of CAP is not new. In fact, it dates back to 1961, when Modigliani & Miller wrote their paper, “Dividend Policy, Growth, and the Valuation of Shares.” In this paper, they asserted that a company’s special investment opportunities would not last in perpetuity, but over some finite interval. They defined CAP as follows:

In his 1997 paper, “CAP – The Neglected Value Driver,” Michael Mauboussin points out that as time goes on, competitive forces drive returns to a level approaching the cost of capital. He graphically illustrates CAP in three figures very similar to Figures 1, 2 and 3 below, where the vertical axis is the percentage of economic profits (return on invested capital less the cost of capital) and the horizontal axis is time. The shaded area under the curve represents the incremental value that management has created for shareholders. As we explain in our paper, “A Valuation Framework for Beating Inflation and Creating Long- Term Wealth,” this is what the market should focus on in order to determine whether or not management creates or destroys value over time.

When creating a discounted Economic Profits Model, investors should estimate how long the CAP will last. To effectively do this, one must assess the competitive dynamics of the industries in which the company competes. The most commonly used framework, and we believe the gold standard for this analysis, is Michael Porter’s five competitive forces. Porter was a pioneer in the development of competitive strategy in his revolutionary 1980 book “Competitive Strategy: Techniques for Analyzing Industries and Competitors.” (Porter, 1980). We intend to dive deeper into the topic of competitive dynamics in our next paper. In the meantime, Porter’s five forces can be summarized as follows:

- Threat of new entrants – the higher the barriers to entry, the longer the CAP and vice versa

- Threat of substitutes – the lower the threat of substitutes, the longer the CAP

- Bargaining power of customers – the lower the customers’ bargaining power, the longer the CAP

- Bargaining power of suppliers – the lower the suppliers’ bargaining power, the longer the CAP

- Industry rivalry – the lower the industry rivalry, the longer the CAP

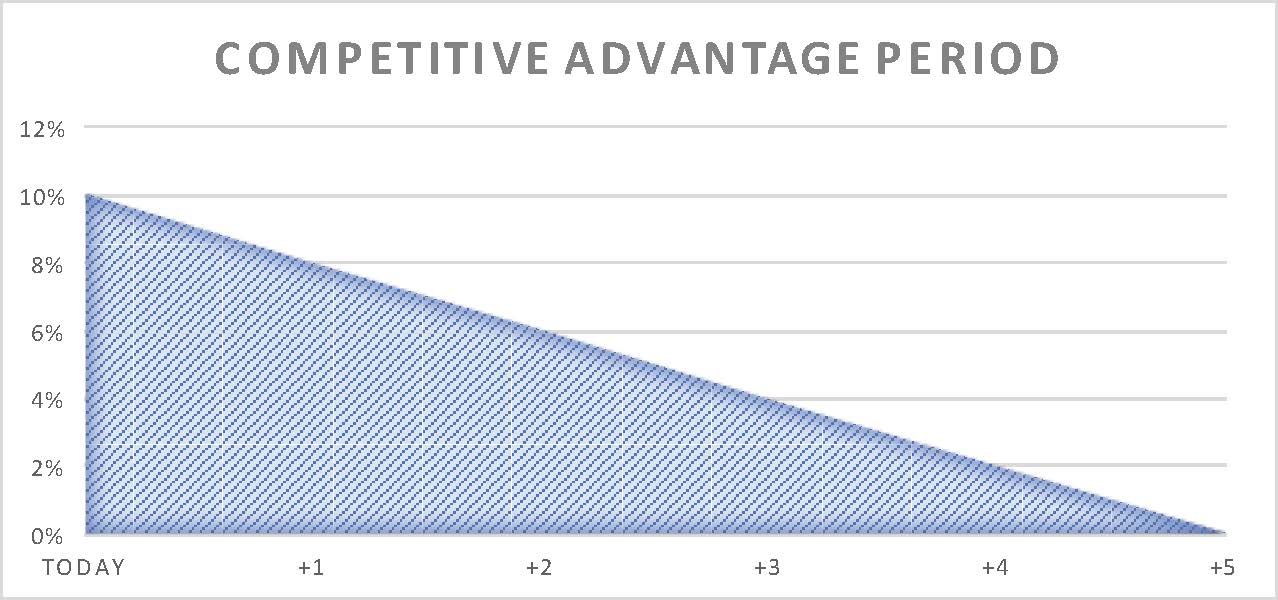

Short Competitive Advantage Period

A Short Competitive Advantage Period (in Figure 1 five years) would be typical for industries that exhibit traits of perfect competition. Perfect competition is a theoretical market structure used as a benchmark against which real-life market structures are compared. In real life, the industry that most closely resembles perfect competition – and would, therefore, exhibit short to no CAP – is agriculture. A farmer goes to market with corn or wheat and takes whatever price the commodity sells for on the exchange. Because the farmer’s crop is identical to all others, the farmer cannot affect the price. No one farmer has a large market share, and no matter how much a farmer sells into the market, it will not change the price. In such a market, it would be difficult if not impossible for any individual farmer to gain any type of competitive advantage versus other farmers. Under perfect competition, there are many buyers and sellers, and prices reflect supply and demand. Consumers have many substitutes if the product or service they wish to buy becomes too expensive or quality falls short. For example, if beef is too expensive, consumers can switch to chicken or pork. Furthermore, new firms can easily enter the market, increasing competition. If corn is more profitable than soybeans, a farmer can switch between plants each year. Companies earn just enough profit to stay in business and no more. If farmers were able to earn excess profits, other companies would enter the market or switch crops and drive profits back down to the bare minimum. If prices remain too low for a period of time, farmers would get out of the market or switch to more profitable crops. Companies that sell commodity type products with no specific attributes will earn no economic profits and operate at or near the industry cost of capital. Thus, their competitive advantage period is virtually non-existent.

Figure 1 – Short Competitive Advantage Period

Source: QSV Equity

Other industries operate with very short CAPs. An example is electronics manufacturing services (EMS). The EMS industry resides at the bottom of the technology supply chain due to low technology differentiation, aggressive bidding for new business programs, and inferior margins. Barriers to entry in EMS are very low, allowing countless competitors across the globe to compete for business. Customers, therefore, hold considerable negotiating leverage and continually demand more services and/or lower prices to retain their business. As a result, EMS firms, such as Sanmina, Flextronics and Jabil, compete largely on price, which limits their ability to improve profitability and earn their cost of capital.

The EMS industry faces a vicious environment where firms are continually required to provide more services for less money. Such unfavorable dynamics keep a ceiling on the profitability potential of competitors within this industry. As a result, many EMS companies find it increasingly difficult to generate returns above their cost of capital. Competitive advantages are very difficult to obtain in the EMS industry, which means that even a five-year CAP might be generous.

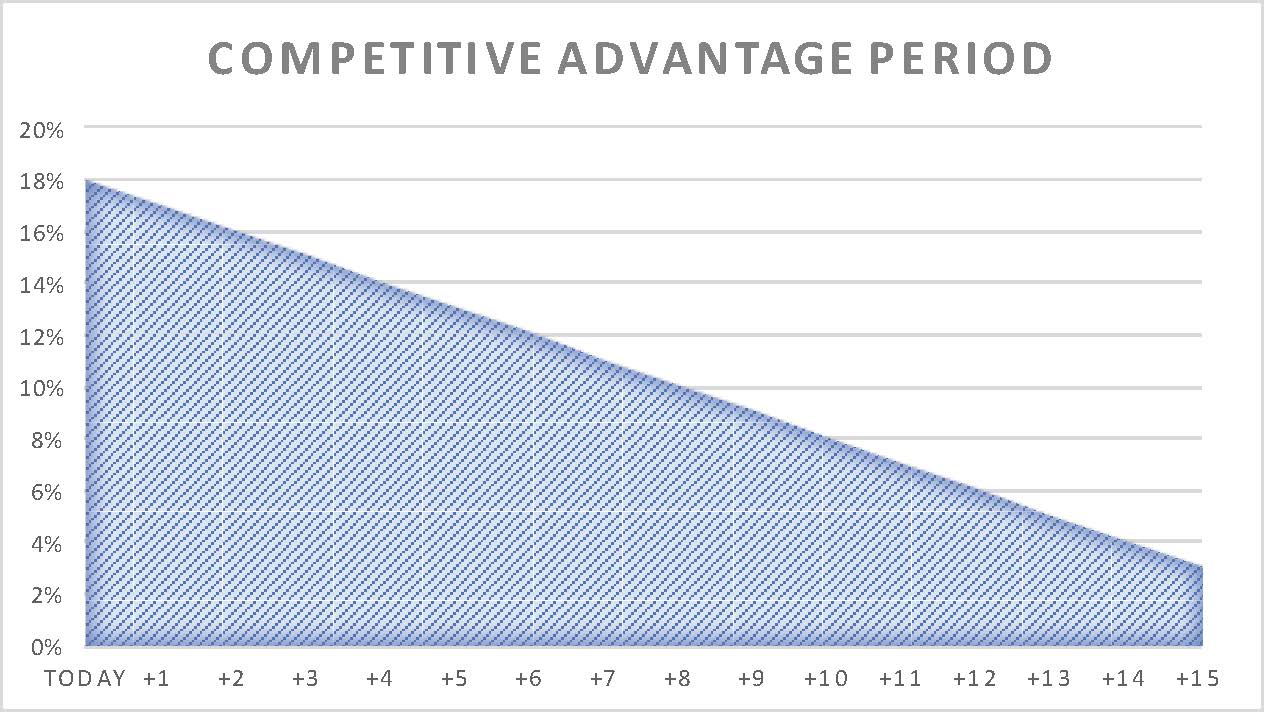

Long Competitive Advantage Period

At the opposite end of the CAP spectrum is a monopoly, where a single company or group owns all or nearly all of the market for a given type of product or service. By definition, monopoly is characterized by an absence of competition, often resulting in high prices and possibly inferior products due to lack of incentive for innovation. There are very few true monopolies in real life. Utilities are considered monopolies if there is only one provider

in a certain area, but even here, government typically regulates what the utility is able to charge. Such

monopolies may enjoy very long competitive advantage periods, but would still achieve slim excess returns above the cost of capital. For individual companies, the best strategy is to position themselves in a profitable industry with some type of advantage to stifle competition.

Figure 2 shows how the CAP may last well into the future if a company possesses a competitive advantage that makes it hard for competitors to copy. The value creation period (shaded area) is much longer for this type of company.

An example of an industry with a long CAP is the system software industry, which exhibits significant competitive advantages due to high switching costs. Companies possess this advantage if buyers face significant inconvenience or expense to change

Figure 2 – Long Competitive Advantage Period

Source: QSV Equity

from their products to another provider. In such cases, a competitor would have to offer substantial improvement in price or performance to motivate users to make a change. Consider how difficult it would be to switch your Microsoft Windows to a competitor’s operating system. It most likely isn’t worth the hassle for any potential savings or expanded capability.

High switching costs are an example of a barrier than can act as a moat, protecting a company from competition. These one-time costs for a buyer switching from one supplier’s product to another’s may include employee training costs, the price of new equipment, time invested in testing or qualifying a new product, need for technical expertise, product redesign, and lost production during a transition from one product to another. The higher these costs, the less prospect of a customer switching to another supplier. This is why customers tend to stick with their current technology and grudgingly pay yearly increases in maintenance or subscriber fees.

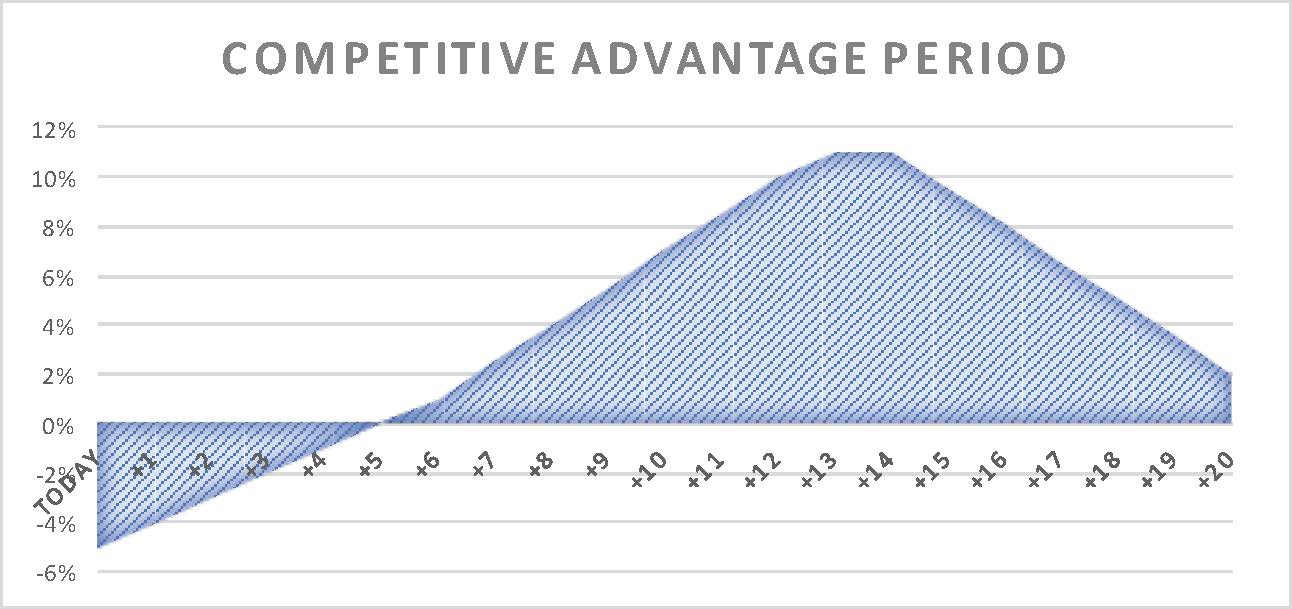

Typical Competitive Advantage Period

In the real world, the CAP period may not be as uniform as the theoretical presentations in Figures 1 and 2. Rather, Figure 3 may be a more realistic representation. A company may have negative economic profits in the early stages as it invests heavily in new projects. Economic profits then eventually turn positive for a number of years as returns on those projects pay off. Then eventually economic profits revert back toward the cost of capital as the company matures or other competitors enter the industry. This is similar to a typical business cycle

Conclusion

In practice, it can be difficult to pinpoint a specific numerical value for CAP. Nonetheless, qualitatively, CAP is extremely useful in the development of financial models. Attention to CAP forces analysts to carefully consider where a company and its industry are in the business life cycle. Awareness of CAP also places greater focus on the competitive landscape. We know that for the vast majority of companies, return on invested capital tends to converge toward their cost of capital over time. Carefully assessing an industry’s competitive landscape and weighing the sustainability of a company’s CAP can greatly improve the efficacy of a valuation model, thereby improving long-term portfolio returns.

Figure 3 – Common Competitive Advantage Period

Source: QSV Equity

Bibliography

Porter, Michael E. Competitive strategy: Techniques for analyzing industries and competitors. Simon and Schuster, 2008.

Miller, Merton H., and Franco Modigliani. “Dividend policy, growth, and the valuation of shares.” the Journal of Business 34, no. 4 (1961): 411-433.

Mauboussin, Michael, and Paul Johnson. “Competitive advantage period: the neglected value driver.” Financial Management (1997): 67-74.