A Quality Upgrade for Mid Cap Investing

QSV is pleased to celebrate another significant milestone, the fifth anniversary of the firm’s Quality Value Midcap strategy. QSV’s founders, Randy Hughes and Jeff Kautz, have managed U.S. mid cap equity portfolios as a team for more than twenty years and believe this asset class to be the “sweet spot” for investors, one deserving of greater attention and, in many cases, larger allocations.

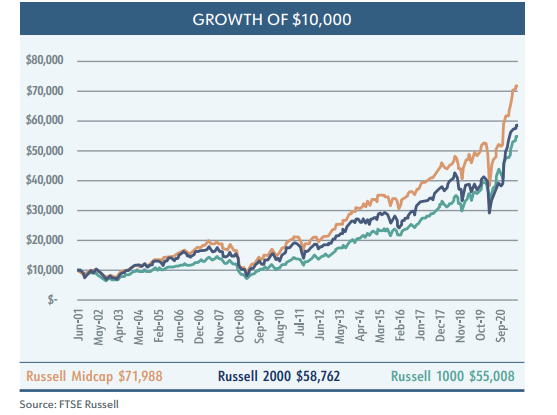

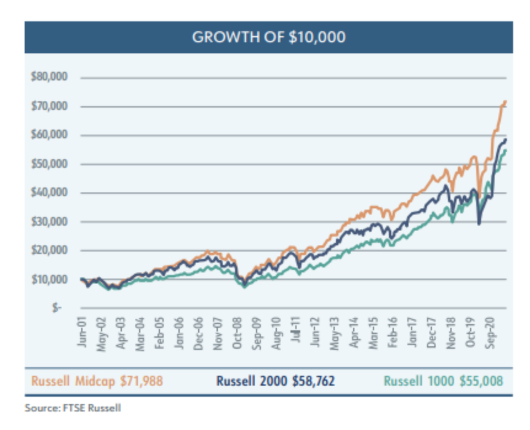

The case for U.S. mid cap stocks has been made before. Relative to large capitalization stocks, mid caps exhibit stronger earnings growth, and offer greater potential returns. Relative to small capitalization stocks, mid caps are more established (reducing the going concern risk), less reliant on having access to capital, less volatile and more liquid. We believe this argument holds merit. Looking at the growth of $10,000 over the previous twenty years, we see that mid cap stocks have outperformed both small cap stocks, represented by the Russell 2000

Index, and large cap stocks, represented by the Russell 1000 Index.

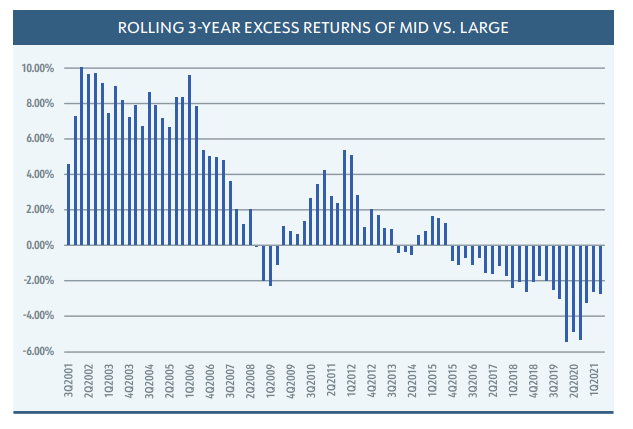

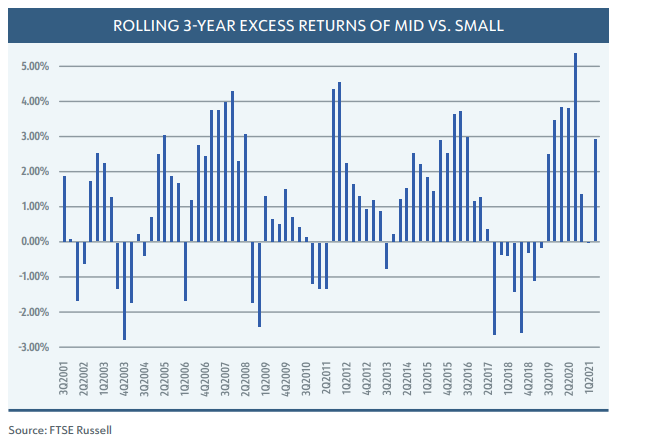

Even if that chart is broken down into periods of rolling three-year returns, we see that mid cap stocks outperform large caps in 63% of those periods and outperform small capitalization stocks in 73% of those three-year periods.

While these numbers alone seem to argue for a greater commitment to mid cap stocks, an even stronger case can be made. By adding a quality overlay to a mid cap strategy, we believe it is possible to structure portfolios that will exhibit 90% upside capture and 70% downside capture. The result being a portfolio that outperforms the market over a full market cycle with less volatility, thereby looking even more appealing on a risk-adjusted basis.

Many investors claim to buy high quality companies. No investor ever admits that they buy low quality companies. At QSV, we have proprietary factor-based scores that we utilize as a starting point to define quality. Companies that exhibit strong returns on invested capital (well in excess of their cost of capital), high free cash flows, high financial flexibility and low capital intensity tend to screen well in our quality rankings. QSV also looks for the presence of a durable competitive advantage, or moat, to help preserve those strong financial characteristics. The combination of these factors is the definition of a high quality company in our investment framework.

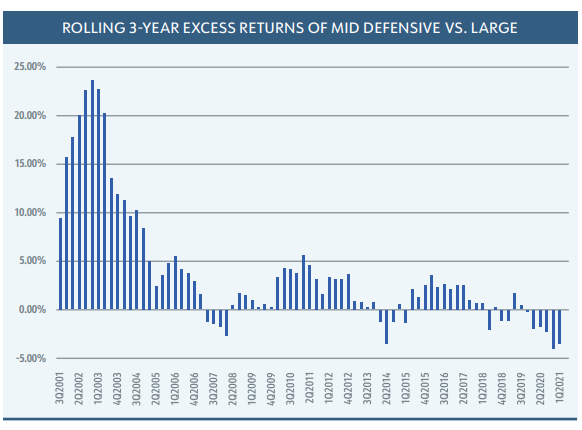

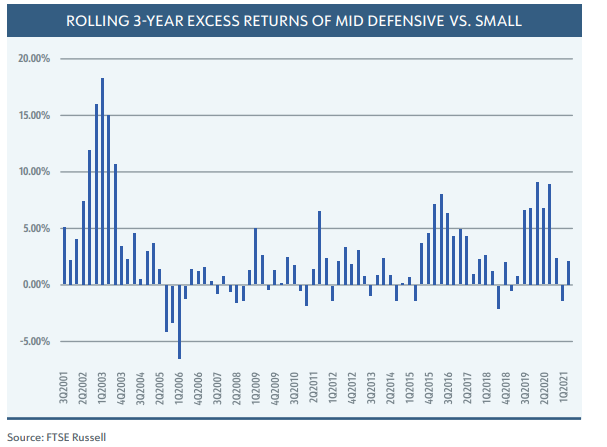

FTSE Russell has done some interesting work with their style-based Stability Indexes, which include a series of defensive and dynamic indices. Russell’s defensive indices utilize a number of the traits we would associate with high quality companies, while their dynamic indices would be what we consider high-beta, lower quality companies. If we look at the same growth of $10,000, what we see is that by adding a quality overlay we can indeed boost the excess return of a portfolio.

Furthermore, by adding a quality overlay, the percentage of rolling three-year periods in which mid cap stocks out-perform increases to 78% relative to large capitalization stocks and to 78% relative to small capitalization stocks.

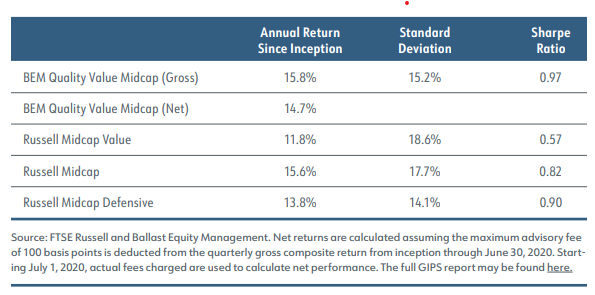

In an environment where artificially low rates are forcing investors to take on more risk to meet their return objectives, we believe that investors would benefit from exposure to high quality midcap stocks in their portfolios. As we look back on our first five years since launching QSV Equity Investors, we believe we are off to a good start in delivering on our promise to investors. QSV Quality Value Midcap strategy has outperformed its primary benchmark while taking on significantly less risk in our clients’ portfolios. This has led to risk-adjusted returns well in excess of our benchmarks as indicated by the Sharpe Ratio of the QSV Quality Value Midcap strategy.

QSV has worked for over 20 years to refine our process of identifying and investing in high quality companies. Our approach requires patience. There will be periods of underperformance, typically coming out of a recession, which we are experiencing now. We do not believe anyone has the ability to consistently time the markets, and we do not attempt to. We believe the better approach is to take a long-term view toward investing that goes beyond simple quarterly or annual returns and focuses on risk-adjusted returns over a full market cycle that includes both peaks and troughs. In doing so, we are confident in our belief that we can outperform our peers and benchmarks and help our clients achieve their long-term financial goals.