Risk Matters

We founded QSV in 2016 to answer the question “how would we want our personal assets to be managed?” With more than twenty-five years of managing client accounts together, we had a philosophy and process in place and knew we could continue to learn and enhance how we invest. A meaningful pillar in our mission statement is to provide a “smoother ride” or the ability for clients to sleep soundly each night without the drama or volatility that some investment styles may deliver. We also founded our business with the belief that attention to risk and setting expectations for clients on how and when we would perform is paramount. QSV’s strategies will not outperform passive benchmarks or our peers in every market environment, but will, we believe, deliver strong risk-adjusted returns and outperformance over full market cycles. Our record to date has proven that to be true.

MEASURING UP (DOWN?)

Tools to evaluate QSV’s performance since the inception of our products include measuring the downside participation that QSV has captured. The downside capture ratio measures how much of the index’s losses a portfolio captures when the market is declining and is calculated by dividing the fund’s returns by the returns of the index during periods when the index is down. In the trailing five years, QSV Mid Cap has delivered downside participation that ranks in the lowest quintile of the Morningstar mid-cap value peer group (rankings sorted from 1st to 100th percentile (with 1st being the highest downside capture to lowest / most favorable in the 100th percentile).

While we strive to improve further on these results, they do reflect well on another pillar of QSV’s mission: to deliver lower drawdowns in challenging markets. Standard deviation of returns is a commonly used measure of volatility to compare an investment portfolio with its benchmark or peers and gives investors a sense of the return “swings” they will endure with a particular portfolio. Here, too, QSV Mid Cap compares favorably with its peers, and ranks in the 86th percentile (with the 100th percentile representing the lowest standard deviation) relative to the Morningstar mid cap value peers. Beta is another tool used to assess the risk of a portfolio. While it is thought that the return potential of a lower beta portfolio is below its benchmark, QSV believes otherwise. In our whitepaper, The Myth of High Beta, QSV questions the long-held belief that higher risk, high beta stocks deliver the highest returns and presents studies that show how the “low volatility anomaly” creates opportunities to beat the market and create long term wealth. QSV Mid Cap has a beta since inception of .73 that ranks in the 90th percentile (with the 100th percentile representing the lowest beta) of the Morningstar Mid Cap Value peer group.

“The lower volatility that QSV has delivered does, we believe, provide the “sleep at night” comfort that many seek.”

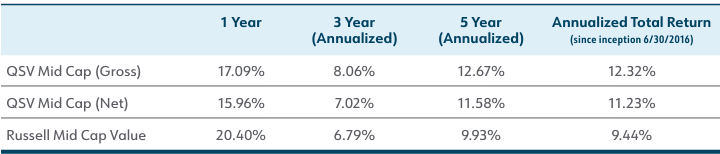

QSV MID CAP PERFORMANCE

These statistics and their relative ranking are important but are only part of the picture. Returns relative to our benchmark matter to our investors, as well, and QSV has delivered outperformance from its inception through March 31, 2024, fulfilling another of our goals.

Based on this performance, one final statistic and ranking to consider is the Sharpe ratio for QSV Mid Cap. The Sharpe ratio divides a portfolio’s returns in excess of a risk-free rate by its standard deviation of returns to assess its risk-adjusted performance. QSV’s since-inception information ratio of .77 ranks in the 9th percentile (where the 1st percentile is the highest Sharpe ratio) of the Morningstar Mid Cap Value peer group, underscoring the risk-adjusted performance we have delivered for our clients.

WHERE DOES QSV FIT?

We believe that the QSV Small Cap, Mid Cap and Select strategies are great core holdings for clients seeking solutions that will permit them to participate in rising markets while protecting in falling markets, resulting in outperformance relative to passive benchmarks over the long term. The lower volatility that QSV has delivered does, we believe, provide the “sleep at night” comfort that many seek. Choices abound and many clients also wish to have small and mid-cap options in their portfolios that may outperform when QSV lags. This typically happens in times such as rapidly rising markets following recessions and periods of stimulative policies, such as we experienced following the COVID pandemic. QSV has been paired by such clients with deep value managers and high-beta growth managers, where, in both cases, our strategies have offset the periods of underperformance by the other and QSV’s portfolios have dampened the overall risk in the clients’ portfolios.

WHERE ARE WE NOW?

In both Q4 2023 and the first quarter of 2024, QSV noted that we felt much of the potential returns for 2024 had been pulled forward in the performance enjoyed in 2023. Markets got ahead of themselves as investors anticipated waning inflation, multiple interest rate cuts by the Federal Reserve, persistent corporate earnings and continued economic growth. Investors awakened in April to the possibility that these expectations may not come true and their change of heart resulted in volatility and a drop in equity markets. While the markets began 2024 with 150 basis points of rate cuts priced in, valuations currently have seventy-five basis points priced in – what the Federal Reserve had communicated in late 2023 and to which investors failed to pay heed until this recent valuation correction.

We believe that mid-cap stocks are attractive for long-term investors, with valuations relative to large capitalization stocks not seen since the late 1990s. The protracted outperformance of large cap stocks has led to underinvestment in small and mid-cap companies; while mid-caps represented 19.7% of the Russell 3000 Index at year-end, the average investor had only a 10.2% allocation, according to Morningstar. With current economic and geopolitical uncertainties, investors should keenly focus on active management and the ownership of quality businesses to build durable portfolios that can withstand the volatility that may continue. A focus on companies that have strong balance sheets and cash flows in today’s environment is critical.

About QSV Equity Investors

QSV Equity Investors, LLC (formerly Ballast Equity Management, LLC) is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices, and institutions. Based in Naperville, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Janus Henderson subsidiary Perkins Investment Management and have invested together for 25 years. For more details on the specific performance and characteristics of QSV’s strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@qsvequity.com.

Disclaimer:

This information is provided solely for informational purposes. Full holdings for the QSV Mid Cap strategy and additional information are available by request at customerservice@qsvequity.com. Morningstar Rankings are relative to the Morningstar Mid Cap Value separate account peer group as of March 31, 2024. Returns are for Mid Cap composite of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Mid Cap Indices as they are a widely used benchmarks for mid capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any

transaction costs, management fees and other expenses, as do QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries the risk of loss. QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. The CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit qsvequity.com. QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at adviserinfo.sec.gov.