QSV Equity Investors

Q3 2023 Commentary

Q3 2023 was difficult for U.S. equities as the reality that “higher for longer” truly will mean higher interest

rates for longer gelled in the minds of investors. The Federal Reserve is intent on fighting inflation and

seems committed to keeping rates high and conditions tight for the foreseeable future, causing concerns

over the impact on the economy. Economic growth and interest rates impact smaller companies more

than large, and small caps experienced a double digit drop from their July peak through the quarter-end.

Three months is a brief period for investors focused on the long term, yet Q3 2023 was a quarter, given

the market environment, where we expected our stock selection in the QSV strategies to perform better.

Particularly within the QSV Small Cap and Select strategies, a handful of companies disappointed. Some

of these, we believe, still deserve a place in the portfolios and we have added to certain names at lower

prices where the disappointment is believed to be temporary. Others we have exited in favor of higher

conviction positions.

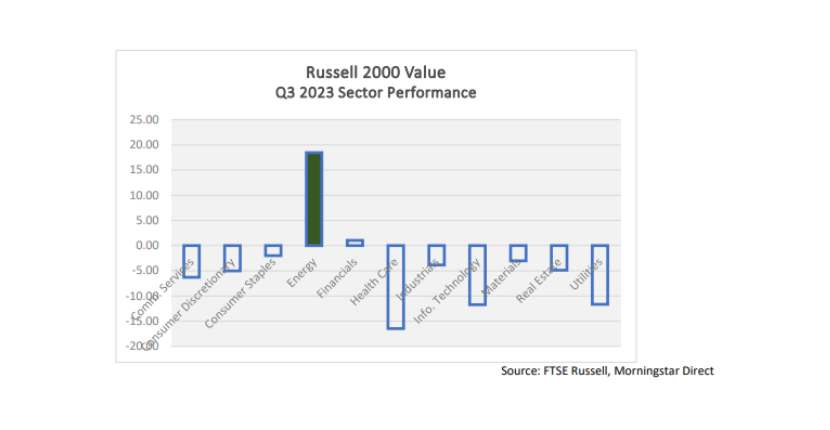

Beyond security selection, the headwinds to our portfolios from being underweight in energy were

considerable this quarter. The Energy sector was up over 18% within the Russell 2000 Value index, while

every other sector – save Financials at +1.04% – were in negative territory. QSV has historically been

underweight in energy companies. In a period of $90 per barrel oil, many energy companies can boast

high returns on invested capital; at more “normal” prices it is challenging to find energy businesses with

competitive advantages, disciplined management, and the high business returns that we require.

QSV’s Small Cap and Select strategies underperformed their respective Russell value indexes during the

quarter while QSV Mid Cap was in line with its index. More information including since-inception

performance for each of the strategies may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned -5.24% and -5.31%, gross and net of fees, lagging the Russell 2000 Value Index

return of -2.96% and the Russell 2000 Index return of -5.13%. The most significant positive impact was

made in Consumer Discretionary companies, where QSV added value in security selection and was

underweight compared to the index, and in Healthcare, where QSV was overweight and added value

through security selection. An underweight and company selection in Energy companies accounted for

nearly all the Small Cap portfolio’s underperformance relative to the index. Company selection in Real

Estate also detracted from relative returns.

QSV Small Cap Top Contributors

Capri Holdings, Ltd. (CPRI) was the leading contributor to performance during the quarter as shares rose

46%. The purveyor of Michael Kors, Jimmy Choo and Versace agreed to be acquired by Tapestry (TPR) for

$57 per share. We expect the deal with TPR to close in 2024 and exited our position placing the proceeds

in companies we believe provide better opportunities.

For the second consecutive quarter, foodservice packaging company Karat Packaging (KRT) was a leading

contributor to performance. Gross margins improved as KRT continued to benefit from lower input and

shipping costs. Core products continue to show sales growth and the company’s Eco-friendly product sales

are trending above 30%. The company initiated a quarterly dividend during the quarter, underscoring the

strength of its free cash flow. KRT generates returns on invested capital of 15%.

QSV Small Cap Top Detractors

After being one of the portfolio’s greatest contributors for the year, shares of Napco Security

Technologies, Inc. (NSSC) dropped on the news that it would restate the prior three quarters’ results due

to understating cost of goods sold. NSSC is a global provider and manufacturer of high-tech security, and

internet-connected home, video, fire alarm, access control, and door locking systems, serving commercial,

industrial, residential, and government markets. Management has said the issue is resolved and will not

impact results going forward. We have concerns about management’s controls that led to the need for

the restatement and will continue to closely monitor the business. Prior to this restatement, we had sold

a meaningful amount of the position on strength.

Forward Air (FWRD) shares were hit on news that they are merging with private company Omni Logistics,

a provider of global freight forwarding and third-party logistics services. The merger will roughly double

the scale of FWRD and will add new growth opportunities with an asset light business, yet it does present

integration risks. QSV acknowledges these risks but sees opportunities for growth and cost synergies

within the business. We added to our position in FWRD on weakness in its shares.

QSV Small Cap Portfolio Activity

The acquisitions of Capri Holdings (CPRI) by Tapestry and PDC Energy (PDCE) by Chevron prompted the

exit of those positions during the quarter. Johnson Outdoors (JOUT), UMH Properties (UMH), and

UniFirst Corporation (UNF) were sold due to business performance that did not meet our expectations

and the opportunity to upgrade to better ideas. New positions were initiated in professional medical

platform Doximity (DOCS), business process management company ExlService (EXLS), LabCorp spin-out

Fortrea Holdings (FTRE), Hanover Insurance (THG), real estate finance company Walker & Dunlop (WD),

and digital media company Ziff Davis (ZD).

QSV Mid Cap returned -4.32%, gross of fees for the quarter, leading the Russell Mid Cap Value Index

return of -4.46% and the Russell Mid Cap Index return of -4.68%. The net return of -4.55% lagged the

Russell Mid Cap Value Index while exceeding the Russell Mid Cap Index. Security selection in Consumer

Discretionary and Industrials companies helped relative performance, while selection in Financials and

Real Estate businesses detracted.

QSV Mid Cap Top Contributors

Outsourced payroll and human capital management provider Trinet Group, Inc. (TNET) was the leading

contributor to performance in the quarter. Increasing use of technology, digitization of the HR function,

employment growth in new industries and increasing geographic decentralization of the small and

medium-sized business workforce all create favorable trends for TNET. TNET has competitive advantages

relative to its peers that include its scale and the efficiencies offered through the consolidation of its

operating units on a single technology platform. TNET generates returns on invested capital of 28% and

shares are at a discount to our estimate of intrinsic value.

Shares of APA Corporation (APA) gained more than 20% during the quarter on rising oil prices,

contributing to the results of QSV Mid Cap. APA produces oil and gas with operations in the U.S., Egypt

and the United Kingdom, and exploration activities offshore in Suriname. APA generates strong free cash

flows and is committed to returning 60% to its shareholders, primarily through share repurchases,

dividends and paying down its debt.

QSV Mid Cap Top Detractors

Masimo Corporation (MASI) fell on poor financial results and lowered future guidance. Results were

impacted by issues that included lower hospital volumes, elevated channel inventory levels, and hospital

labor inflation that is impacting capital equipment demand. MASI is a medical technology company which

develops, manufactures, and markets non-invasive vital sign monitoring devices and offers consumer

audio products. The integration of its acquisition of Sound Audio has continued to present challenges to

the business and we exited the position in favor of higher conviction businesses.

Etsy Inc. (ETSY) detracted from performance during the quarter. Etsy markets differentiated products

through its “House of Brands” which includes Esty.com, Reverb, and Depop. Competitive advantages

include the diversity of its offerings, a strong base of active buyers and sellers, and productivity tools it

offers sellers. Despite these advantages, with rising fuel prices, the resumption of student loan payments,

and a shift by consumers to “experiences” over goods, we believe there are better opportunities for our

investors, thus we exited the position during the quarter.

QSV Mid Cap Portfolio Activity

Turnover during the quarter was higher than usual as QSV took opportunities to upgrade its portfolio. As

noted above, Etsy (ETSY) and Masimo (MASI) were exited for business performance reasons. A.O. Smith

(AOS), Cintas (CTAS), and Ross Stores (ROST) were sold for valuation reasons and Mid-America

Apartment Communities (MAA) was sold to allocate to better ideas. New positions were initiated in

digital services provider Amdocs (DOX), nitrogen producer CF Industries (CF), LabCorp spin-out Fortrea

Holdings (FTRE), GPS-enabled hardware and software provider Garmin (GRMN), Match Group (MTCH),

elevator and escalator manufacturer OTIS Worldwide (OTIS), and Waters (WAT), a provider of liquid

chromatography and mass spectrometry products.

QSV Select returned -6.25% and -6.45%, gross and net of fees, lagging the returns of -3.66% and -4.78%,

respectively for the Russell 2500 Value and the Russell 2500 Indexes. Select is a high conviction strategy

that takes QSV’s best ideas from our Small Cap and Mid Cap strategies. An underweight and company

selection in Consumer Discretionary companies helped performance as did QSV’s absence in the poorly

performing Utilities sector. Company selection detracted from performance in the Financials sector as did

our underweight and underperformance in Energy businesses.

QSV Select Top Contributors

Brady Corporation (BRC) was the leading contributor to performance during the quarter as the company

beat consensus earnings estimates and raised its guidance for the full year. The company manufactures

and sells identification and workplace safety products through its Identification Solutions and Workplace

Safety segments. BRC has niche advantages in safety, identification, and compliance markets and has a

diversified customer base, products, and geographic footprint. The company’s strong free cash flows have

supported dividend increases for thirty-seven consecutive years, share buybacks and strategic

acquisitions.

EPAM Systems, Inc. (EPAM) rose as quarterly results were better than anticipated. The company has

diversified its workforce away from its previous exposure to Ukraine and the belief that demand for the

company’s services may be bottoming raised investor sentiment. The global technology services company

has a network of multidisciplinary teams delivering software product development and digital platform

engineering services. Most of the firm’s revenues are generated from U.S. customers and its top twenty

clients (representing 41% of revenue) have been with EPAM for an average of ten years. Returns on

invested capital stand at 17%.

QSV Select Top Detractors

Masimo Corporation (MASI) and Napco Security Technologies, Inc. (NSSC) were the leading detractors

from performance in Q3 and are discussed above.

QSV Select Portfolio Activity

QSV took opportunities to upgrade the Select portfolio during the quarter. Shares of PDC Energy (PDCE)

were sold as Chevron (CVX) acquired the business. Generac Holdings (GNRC) was sold for valuation

reasons. Positions were initiated in CF Industries (CF) and Fortrea Holdings (FTRE).

Our Focus on the Long Term

Investors began the last quarter on an optimistic note, while bullishness faded in September. Strength of the

consumer continues to be touted as a positive for the economy (Americans Are Still Spending Like There’s No Tomorrow), as are strong employment and rising labor participation rates. Yet credit card debt is high

and student loan payments are again due. Persistent inflation and higher interest rates will also weigh on

the consumer as well as on corporate earnings. The Financial Times notes that 30% of the debt of Russell

2000 companies is variable rate debt (as compared to 6% for S&P 500 companies), presenting risks to lower

quality, more leveraged businesses.

At this stage in the market cycle, we believe that QSV’s style of investing and our investors should do well.

Late cycle investing favorsthe lower volatility stocks of quality businesses, those that have limited debt, high

interest rate coverage and strong free cash flows. Selectivity is important and opportunities abound in small

to mid-cap stocks that have been overlooked in the narrow market that dominated the first half of the year.

Investors will also do well to check their asset allocation; the mega-cap led markets of 2023 have left many

portfolios in an unbalanced state and shifts in allocations may be due.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of

trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All

dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the

historical performance of the Russell 2000 Indices as they are a widely used benchmarks for small

capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical

performance of the Russell Midcap Indices as they are a widely used benchmarks for mid capitalization

securities. The returns of the QSV Select strategy are compared to the historical performance of the

Russell 2500 Indices as they are a widely used benchmarks for SMID capitalization securities. An

investment with QSV Equity Investors should not be construed as an investment in a program that seeks

to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these

indices. Furthermore, these indices do not include any transaction costs, management fees and other

expenses, as do the QSV products. Lastly, QSV may invest in securities and positions that are not included

in these indices.

No client or potential client should assume that any information presented should be construed as

personalized investment advice. Personalized investment advice can only be rendered after engagement

of the firm for services, execution of the required documentation, and receipt of required disclosures.

Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®).

GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this

organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS

report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm

and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.