The Trouble with Point Estimates

The Trouble with Point Estimates

QSV_The Trouble with Point Estimates

NEW BRAND. SAME PEOPLE, PHILOSOPHY AND PROCESS.

The Ballast Equity Management team has worked together for over 25 years, refining our investment philosophy and process, and improving our craft. Our skillset is in researching, valuing, and building portfolios of small and mid-cap stocks and decidedly not in marketing or branding, thus we find ourselves with a corporate name, Ballast Equity Management, which is quite like that of another, peer, firm. As a result, we are rebranding our firm to QSV Equity Investors. QSV stands for the Quality, Stability and Value that we continually seek to deliver to our clients with each decision we make. Our people, philosophy and process will not change, only our name will.

THE TROUBLE WITH POINT ESTIMATES

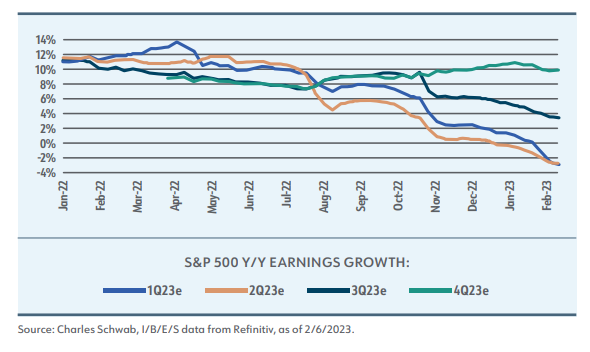

After an era of low interest rates, globalization and low inflation, investors were hit in 2022 with the reality of a new regime, one marked by higher interest rates, inflation, and higher volatility. This new regime has percolated its way into corporate earnings with negative earnings surprises notable in the Communication Services, Information Technology, and Consumer Discretionary sectors. Where earnings for the market go in the near term is difficult to predict, but consensus is that these declines are likely to continue into the next quarter and, we believe, the consensus view may be too rosy for the balance of 2023. At QSV, we worry about the “E” in P/E and feel the game has gotten more challenging for investors seeking to make quick decisions based on the point estimates often used in valuing stocks.

ALL VALUATION TOOLS ARE NOT EQUAL

Point estimates, or market multiples, are widely used by investors and Price to Earnings is the most often used tool for valuing equities. P/E is simple to use, requiring just two inputs. The trailing 12-month price-to-earnings multiple, for example, divides a stock’s current share price by the last year’s earnings per share. The simplicity of this calculation also speaks to its shortcomings– multiples tend only to provide high-level snapshots of valuation at a point in time. These limitations can misguide investors; a P/E may appear low because the company is at peak earnings. Or, without considering what may happen to the “E,” or earnings, in such a simple equation, investors often can step into value traps – stocks that are cheap for good reason – when relying on multiples. Though investors can gain more insight by looking at a company’s P/E multiple over many years or by comparing it to the market and other companies in the same industry, there is another critical drawback; valuation multiples still do not account for cash and debt on the company’s balance sheet. More importantly, they do not account for a company’s potential growth or its risk profile. Because of such limitations, we at QSV may use these ratios in our initial screening process, but we rely on a more robust model to derive our ultimate intrinsic value estimates.

QSV relies on a proprietary, and more sophisticated, valuation model to identify winning companies. Our Economic Profits model enables us to take a closer look at what a prospective firm has going on under the hood. Economic Profits and Discounted Cash Flow (DCF) models are similar and should arrive at the same intrinsic value for a company. However, we believe the Economic Profits model, which considers both the cost of debt, as DCF does, as well as the cost of equity, provides additional insight. By studying the firm’s capital structure and allocation decisions, such as its debt levels, tax rates, share repurchases and dividend payouts, QSV can assess whether management’s capital allocation decisions are creating or destroying value, making this model a more comprehensive tool for valuing a firm’s stock.

FUNDAMENTALS IN FOCUS

Before the valuation process begins, QSV conducts thorough quantitative and qualitative analysis to seek out businesses with competitive “moats.” We believe that business performance, including high margins, reverts to the mean over time, but we also believe that competitive advantages enable companies to maintain higher than average performance for longer periods of time. High quality companies tend to remain high quality companies. This persistence helps us value the stocks of these companies with a higher degree of conviction.

Easy money and rising markets created wealth and nascent investment success in areas that would never have occurred to Ben Graham or Warren Buffett at the beginning of the post-financial crisis era. Passive investing made a great percentage of active managers look passé. Meme stocks made work from home traders temporarily wealthy. Thematic ETFs focused on these meme stocks, on our politicians’ personal trading, and on other “disruptive” ideas capitalized on investors’ optimism, yet often went from hot to cold with startling speed. In the current environment of greater uncertainty, higher borrowing costs, and earnings headwinds, we believe investors would be prudent to emphasize active management in quality businesses, those with durable competitive advantages, strong balance sheets and strong and growing free cash flows.

About QSV Equity Investors

QSV Equity Investors (formerly Ballast Equity Management) is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Perkins Investment Management and have invested together for over 20 years. For more details on the specific performance and characteristics of QSV’s strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@qsvequity.com.